Category: Financial & Tax Planning

Date: March 31, 2024

The predictability and permanence of any federal transfer tax (estate, gift, GST) laws are inherently low, and this has never been more true than it is in the current political landscape. Fluctuation around exemptions, tax rates, portability, and other related issues has been significant over the last two decades, and we are nearing the precipice of another such wholesale change.

The 2017 Tax Cuts and Jobs Act (“TCJA” and often referred to as the “Trump Tax Cuts”) brought sweeping changes to the tax code, and TCJA specifically changed the transfer tax rules temporarily (through the end of 2025) by effectively doubling the combined gift and estate tax exemption to $10mm (based on 2017 values and adjusted annual for inflation) with a top rate of 40% for gifts and estates exceeding the exemption. In 2024, that exemption is $13.61mm ($27.22mm for married couples). An important feature of the TCJA is its built-in legislative sunset at the end of 2025, meaning that if Congress does not proactively do anything prior to Jan 1, 2026, the exemption will revert to the transfer tax regime in place prior to the passage of TCJA. Indeed all of the so-called Trump Tax Cuts would sunset in 2026.

Given the dysfunction in our Congressional landscape, many practitioners agree that the most reliable assumption is that TCJA’s built-in sunset will run its course. As such, the 2017 tax act would see the 2026 exemption roll back to $5mm indexed for inflation (estimated to be approximately $7.0mm by many). It should be noted that the IRS has issued final regulations confirming that IRS attempts to recapture or clawback any otherwise permissible gifts will not apply. So a gift made prior to 2026 for an amount in excess of the 2026 exemption thresholds will not be subject to clawback or recapture by the IRS.

Questions around what to do in the face of these issues have been increasingly on the lips of tax practitioners and wealthy individuals really since 2018, with the looming election and soaring interest rates being factors that have ratcheted up the stakes. Gifts of $7.0mm (the projected 2026 exemption amount) or less gifts don’t really move the needle, because the gifted amount would come “off the bottom” if/when the exemptions sunset. Some common gift techniques being discussed are SLATs, QPRTs, and other irrevocable trust techniques.

A lot of transfer tax planning is at the nexus of what the math says you CAN do and what your goals and concerns dictate what you SHOULD do. This has never been more true for people who fit a profile that is not uncommon in our firm’s conversations. Specifically, for a married couple with a combined net worth closely approximating the current amount of a married couple’s combined estate tax exemption (but would have an estate in excess of the 2026 exemptions in the event of the TCJA sunset occuring).

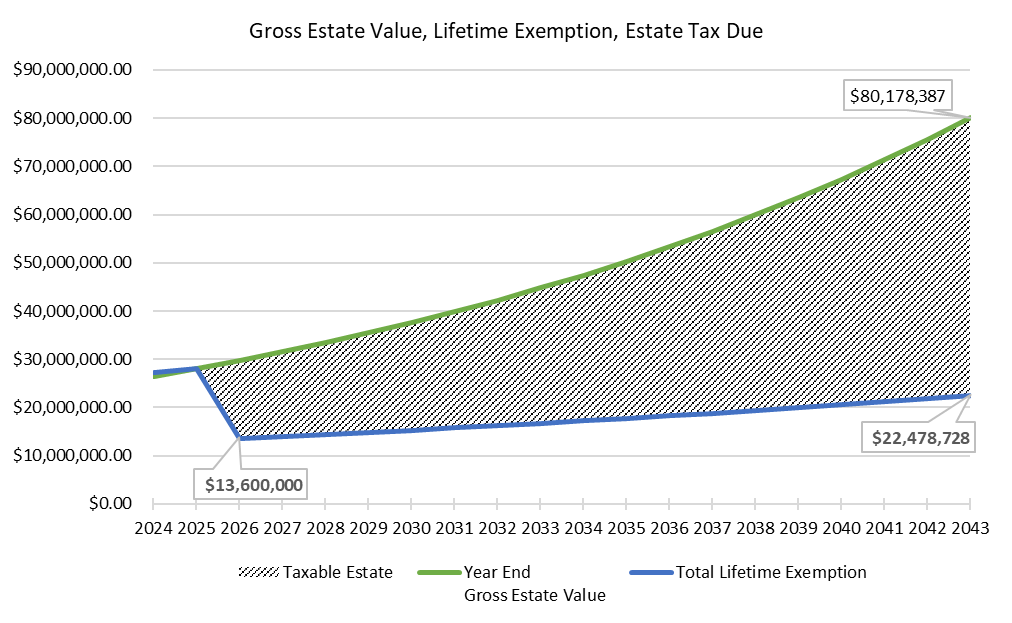

Let’s examine the impact for a hypothetical HNW couple, Betty and Barney Rubble. Betty and Barney have a combined taxable estate of $25,000,000 at the beginning of 2024. Their combined wealth is expected to grow annually at 3% (net of inflation, and net of all expenses including lifestyle, debt service, income taxes, etc). If the Rubbles do no planning before they die, the results could be pretty dire for their son, Bam Bam. The chart below illustrates how dramatically the impact will be for the Rubble family if the estate tax exemption sunsets in 2026. Over the next 20 years, the situation worsens. The shaded area between the green line (the Rubble family’s taxable estate) and the blue line (their combined lifetime exemptions) represents the portion of their estate that will be exposed to a 40% estate tax rate.

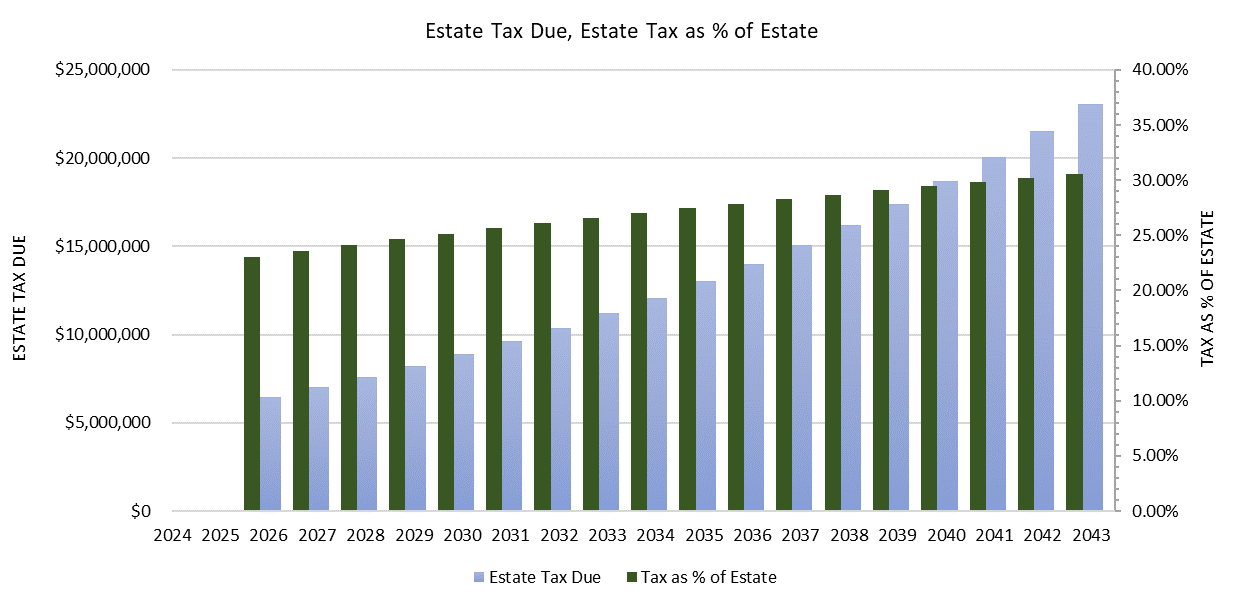

And to further underscore the cost of delay, the next graph illustrates the cost beginning in 2026. The blue bar is the estate tax liability in dollars and measured by the left axis. The green bar is the % of the Rubble family estate that would be eroded by estate taxes, seen on the right.

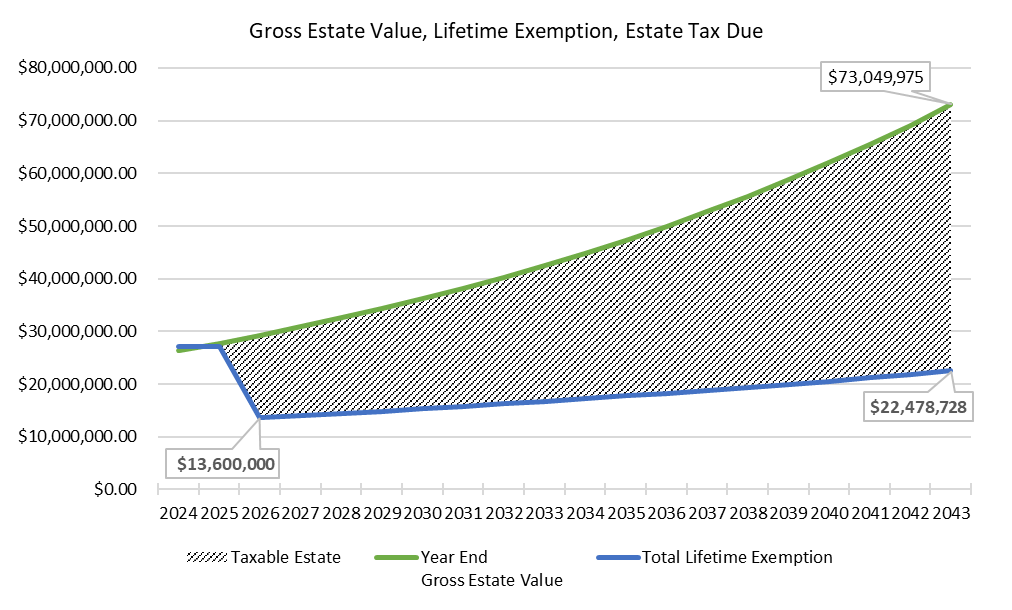

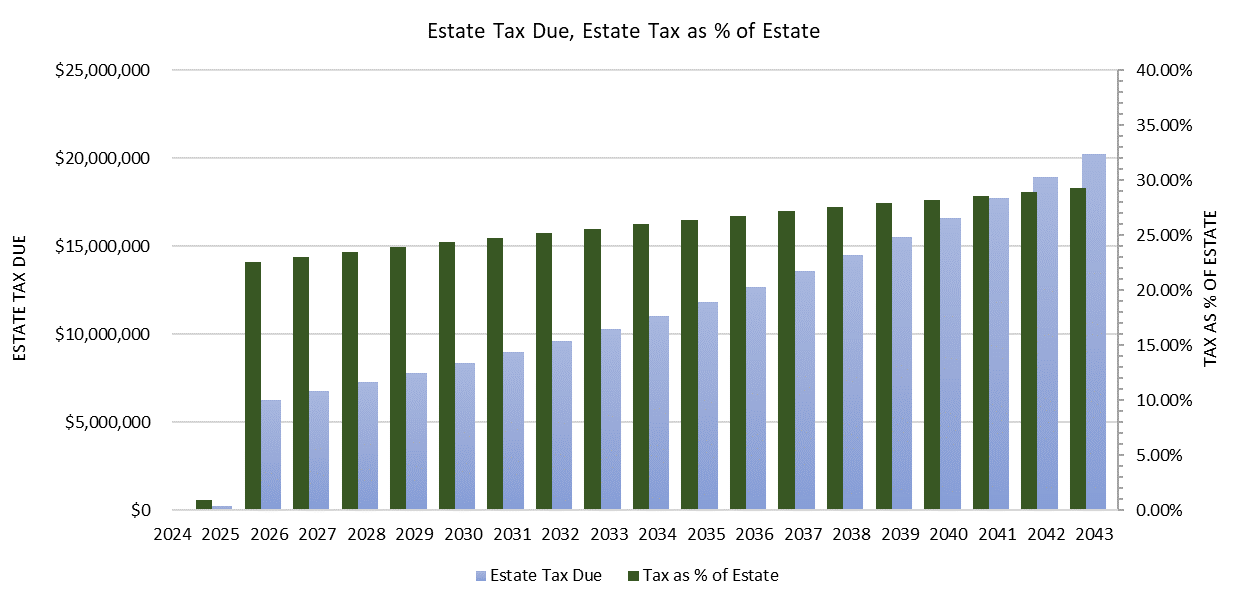

Let’s review another family in a similar situation. Fred and Wilma Flintstone have a nearly identical net worth and situation. Like their friends, they also delay making any decisions. Instantly in 2026, they experience remorse at the situation and decide to embark upon a gifting program to provide annual exclusion gifts ($18,000 per year) to their daughter, Pebbles, and her husband and two children. That allows them to make $144k in gifts (2 donors x 4 donees x $18k) per year. The impact over 20 years of that gifting program can be significant. The next two charts highlight something as simple as a gifting program to whittle away at the estate.

Comparing Illustration 1 to 3, you can see that the result is to transfer over $7 million of value over 20 years. The impact is an estate tax savings of almost $2.9 million.

There are a number of things that a HNW family could do now to address these consequences in far more meaningful and dramatic fashion. At the end of the day, there are only three potential destinations for the assets of a deceased person: the people we love, the charities we care about, and the federal government. There is no fourth option.

But there are ways to solve for accentuating the first two and mitigating the third. As one of my partners, Luther Lockwood, is apt to say: “consumption is a great estate tax strategy.” And proper planning with various lifetime gifting strategies before the end of 2025 will be a crucial element to consider. Benjamin Franklin once wrote “An ounce of prevention is worth a pound of cure.” The context for the statement was in warning to Philadelphians of the potential risk of waste due to fire hazards. Similarly, in the context of avoidable estate tax liabilities, an ounce of gift tax planning now can avoid a large estate being consumed by avoidable and wasteful estate taxes. Our paper from 2022 on SLATs is a good starting point!

Summary and Conclusion

The TCJA has been a huge windfall since 2018 for wealthy families’ opportunities for estate and gift tax planning. That window of opportunity is closing unless Congress does something about it. While we are constantly reminded of how we have zero control over what politicians do, we can control how prepared we are for the potential impact of dramatic, negative changes to the federal estate tax regime. The clock is ticking and given that many families are going to be in the same position, procrastination could be very detrimental. Careful planning takes time, and you don’t want to be the one caught without a chair when the music stops.

This material and the opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual or entity. To determine what is appropriate for you, please contact your personal advisors. Information obtained from third-party sources are believed to be reliable but not guaranteed.

The tax and legal references attached herein are designed to provide accurate and authoritative information with regard to the subject matter covered and are provided with the understanding that MBL Advisors is not engaged in rendering tax, legal, or actuarial services. If tax, legal, or actuarial advice is required, you should consult your accountant, attorney, or actuary. MBL Advisors does not replace those advisors. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional before implementing such strategies.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. For important information related to MBL Wealth, LLC, refer to the Client Relationship Summary (Form CRS) by navigating to https://mbl-advisors.com. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. For important information related to M Holdings Securities, Inc, refer to the Client Relationship Summary (Form CRS) by navigating to https://mfin.com/m-securities. Insurance solutions are offered through MBL Advisors Inc.

Form#5079618

This material and the opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual or entity. To determine what is appropriate for you, please contact your personal advisors. Information obtained from third-party sources are believed to be reliable but not guaranteed. The tax and legal references attached herein are designed to provide accurate and authoritative information with regard to the subject matter covered and are provided with the understanding that MBL Advisors Inc., is not engaged in rendering tax, legal, or actuarial services. If tax, legal, or actuarial advice is required, you should consult your accountant, attorney, or actuary. MBL Advisors Inc., does not replace those advisors. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional before implementing such strategies.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. For important information related to MBL Wealth, LLC, refer to the Client Relationship Summary (Form CRS) by navigating to http://mbl-advisors.com. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. For important information related to M Holdings Securities, Inc, refer to the Client Relationship Summary (Form CRS) by navigating to https://mfin.com/m-securities. Insurance solutions are offered through MBL Advisors Inc.