Category: Financial & Tax Planning

Date: April 15, 2026

Last quarter my partner Billy Morton covered some of the details necessary to create a buy-sell agreement. As a follow-up we wanted to provide a deeper dive into funding a Buy Sell Agreement with some actual case studies that may be helpful to further understand the concepts. A buy-sell plan provides protection for the business to continue based on a number or circumstances. Our focus will be on the primary unforeseen triggers for buy sell agreements of death and disability of a shareholder of the business.

A buy-sell agreement is more of a contingency plan than a succession plan and provides a blueprint in case of emergency. A well-structured plan will benefit all parties involved by providing a smooth transition for converting illiquid privately held stock into cash. The surviving shareholders will be able to continue the business or have the option to possibly use some of the insurance proceeds to buy enough time to find an interested buyer. The insurance proceeds can provide full value of the business for the estate/heirs of the deceased shareholder to provide income for survivors, estate settlement costs and possible estate taxes.

Most Buy Sell Agreements fall into one of two categories: Stock Redemption Plan (sometimes called an Entity Purchase Agreement) or a Cross Purchase Plan with a few variations.

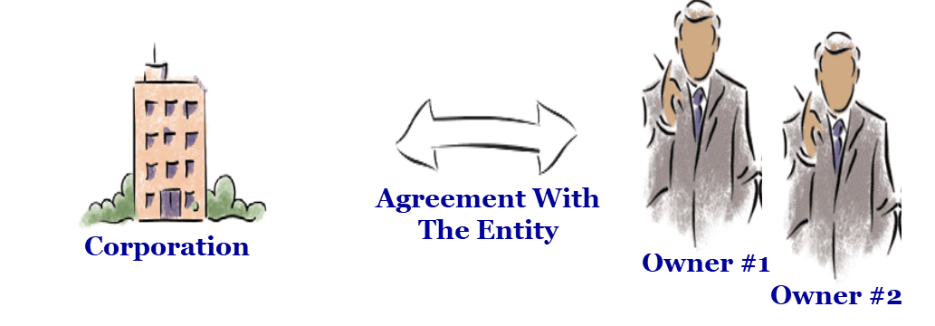

Stock Redemption Plan

In a Stock Redemption plan the Company (entity) buys the insurance on each shareholder and is the beneficiary of the policy. Premiums paid by the Company are not tax deductible but policy proceeds (life insurance death benefits and disability benefits) are not taxable income as long as the participant as agreed to be insured.(1) Upon a triggering event the Company receives the policy proceeds and redeems (purchases) the outstanding stock. The redeemed shares are retired as treasury stock and not reissued. The remaining shareholders own a larger percentage of the business but their cost basis remains the same.

Case Study

After a lengthy interview process by a consulting firm, MBL Advisors was engaged by an international distribution company to place $300 million of life insurance to fund a buy-sell plan for seven major shareholders. The consultant required that the coverage should be split with two or three carriers for each shareholder. The firm was able to leverage the underwriting results to create competition among carriers to obtain the best results for the Company. Each shareholder engaged outside counsel to review the plan in addition to corporate counsel.

Disability and Life Insurance Case Study

The firm was referred to a national wholesale distribution company by a board member after successfully completing a management buy out. Based on the arrangement only active employees could be shareholders in the Company. The Company was in debt and did not want to take on additional debt to repurchase stock from a disabled or deceased shareholder. We designed a plan to purchase $96M of disability buy out coverage on the top ten executives through Lloyd’s of London. The policies will pay a lump sum disability benefit to the Company after a one year elimination period (waiting period) to provide the Company a tax free benefit to redeem the stock of the disabled executive. The first $1.5M of coverage was issued on a Guaranteed Standard Issue basis without medical underwriting. The Company concurrently purchased life insurance policies on the same executives using the same medical information to make it more convenient for each executive.

The Stock Redemption Plan was the best option in these cases.

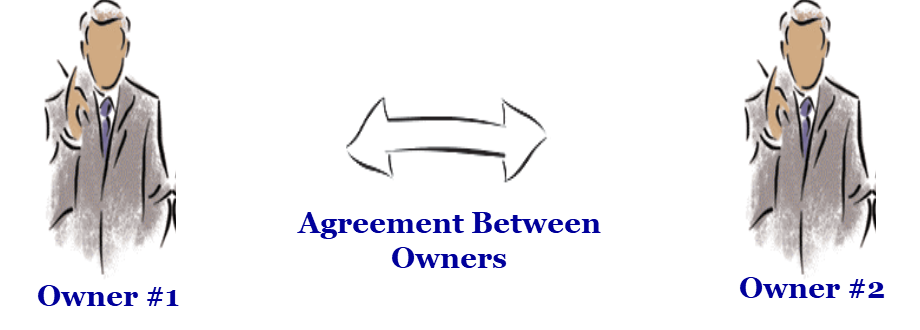

Cross Purchase Plan

In a cross purchase plan each shareholder purchases a policy on the other individual shareholders. The shareholder is the policyowner and beneficiary of the coverage and the Company bonuses the premiums annually. In the event of a claim the individual shareholder receives the insurance benefits on a tax free basis and uses the proceeds to buy the outstanding stock from the estate of the deceased. The surviving shareholder receives an increase in cost basis that can reduce future capital gains on a subsequent sale of the business. When the business has more than two owners the number of policies needed to fund a Cross Purchase Plan can become problematic. With two shareholders only two policies are required. With three shareholders six policies are required (each shareholder buys a policy on the other two). Four shareholders would need to buy a total of twelve policies (three policies per shareholder) so most elect a Stock Redemption plan.

Case Study

The firm was referred by a corporate attorney to a textile manufacturing company with a recent valuation of $24 million. The company had three shareholders with an equal ownership percentage of the business. The shareholders used the cross purchase method to purchase two $4 million policies on each shareholder. The shareholders were similar in age so the premiums were relatively similar. The Company bonused each shareholder the annual premium for each policy to fund the plan on an ongoing basis.

Alternative Situation Case Study

A healthcare services company received an updated valuation from an investment banker showing a current valuation of $200 million. The business had two equal shareholders who were considering selling the business in the next three to five years. As an alternative to funding the full valuation with life insurance the shareholders agreed to purchase $20 million on each partner in a cross purchase arrangement. The logic behind the $20 million is it would be enough for the surviving partner to buy enough stock to be majority owner and hire additional resources to help run the business until it was stable enough to be sold. Neither owner wanted to be forced to sell in a fire sale scenario.

In closing, a Stock Redemption plan is popular in larger businesses with multiple owners because only one policy is needed to fund the plan and in situations where there is a significant difference in premiums (owners are from different generations or health issues). The long term benefit of a step up in cost basis is the most compelling reason to use a Cross Purchase plan. A number of variations may be appropriate based on the specific goals of the shareholders.

- The Employer must meet the notice and consent requirements of IRC Section 101(j) and reporting requirements of IRC 6039I.

Case study results are for illustrative/informational purposes only and may not reflect the typical purchaser’s (client’s) experience and are not intended to represent or guarantee that anyone will achieve the same or similar results. This material and the opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual or entity. To determine what is appropriate for you, please contact your personal advisors. Information obtained from third-party sources are believed to be reliable but not guaranteed. #5281694

The tax and legal references attached herein are designed to provide accurate and authoritative information with regard to the subject matter covered and are provided with the understanding that MBL Advisors is not engaged in rendering tax, legal, or actuarial services. If tax, legal, or actuarial advice is required, you should consult your accountant, attorney, or actuary. MBL Advisors does not replace those advisors. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional before implementing such strategies.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. For important information related to MBL Wealth, LLC, refer to the Client Relationship Summary (Form CRS) by navigating to https://mbl-advisors.com. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. For important information related to M Holdings Securities, Inc, refer to the Client Relationship Summary (Form CRS) by navigating to https://mfin.com/m-securities. Insurance solutions are offered through MBL Advisors Inc.

This material and the opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual or entity. To determine what is appropriate for you, please contact your personal advisors. Information obtained from third-party sources are believed to be reliable but not guaranteed. The tax and legal references attached herein are designed to provide accurate and authoritative information with regard to the subject matter covered and are provided with the understanding that MBL Advisors Inc., is not engaged in rendering tax, legal, or actuarial services. If tax, legal, or actuarial advice is required, you should consult your accountant, attorney, or actuary. MBL Advisors Inc., does not replace those advisors. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional before implementing such strategies.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. For important information related to MBL Wealth, LLC, refer to the Client Relationship Summary (Form CRS) by navigating to http://mbl-advisors.com. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. For important information related to M Holdings Securities, Inc, refer to the Client Relationship Summary (Form CRS) by navigating to https://mfin.com/m-securities. Insurance solutions are offered through MBL Advisors Inc.