Category: Financial & Tax Planning

Date: July 22, 2024

Category: Financial & Tax Planning

Why are we writing about tax loss harvesting in June – in an up market at record highs no less? Shouldn’t this be published in November or December?

Many investors and financial advisors treat the notion of tax loss harvesting as an event that should be done once a year in December, like the payment of taxes in April (or October) or the administration of a required minimum distribution from an IRA. The routine for many investors is to harvest losses in December. But end-of-year loss harvesting could mean missed opportunities.

For an investor, many factors might contribute to the notion that tax-loss harvesting should be an annual event in December rather than a disciplined process. The emotional aspect of investing (sometimes referred to as “Behavioral Finance”) certainly plays a role too. Most investors have “a deeply ingrained aversion to realizing losses.”1 Another aspect is the reality that differentiates the taxation of long-term versus short-term gains. That distinction might bleed over into how an investor also thinks about losses. But the good rule of thumb is that whenever possible, an investor should realize gains, if at all, only when they become long-term, but realize losses as soon as practicable. This mantra would help combat the irrational tendency that exists for many investors to hold onto their losers (in hopes they will recover) and sell their winners too early. “An effective taxloss harvesting strategy has the benefit that it can reduce this behavioral bias.”2

All of these are reasons that an investor might delay or defer. But, as Paul Unchalipongse from Columbia Threadneedle writes, “when December rolls around, they’re out of patience and their frame of reference switches: it feels like a good time to claim the tax deduction of a realized loss. The most common reasoning behind December loss harvesting is based on emotion and simple convenience, rather than strategic thinking.”3

For an investment advisor, the short-sightedness of this approach could be both misguided and costly to his or her clients. But it is very telling about the nature of many advisory practices that believe their roles are transactional in nature rather than relational in nature. We believe that tax loss harvesting is a crucial aspect to the long-term success of a taxable portfolio and is at the very fabric of our investment philosophy. A mentor of ours used to 1 say that there are only two predictable forms of alpha, and they are both negative: fees and taxes. While many of our peers may view harvesting tax losses as something they do in the 4th quarter, the notion of tax efficiency is central to our core investment philosophy at MBL Advisors. To be sure, we never allow the proverbial tax tail to wag the investment dog, but investment management without proper consideration of tax implications is akin to living in a vacuum and is a luxury that does not exist outside the world of academia.

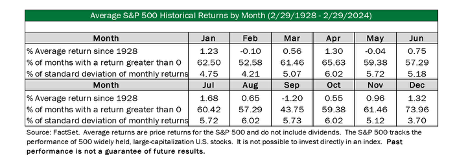

The chart below highlights why treating tax-loss harvesting as a December-only event may actually be a detrimental approach for investors. First, because it shouldn’t be an event instead of a process as already discussed. And second, if one does treat it as a once-a-year event, December would be the worst month of the year to harvest losses, from a statistical perspective.

Source: FactSet. Average returns are price returns for the S&P 500 and do not include dividends. The S&P 500 tracks the performance of 500 widely held, large-capitalization U.S. stocks. It is not possible to invest directly in an index. Past performance is not a guarantee of future results.

As the chart above demonstrates, December experiences a positive market return 74% of the time. Coupled with also having the lowest standard of deviation relative to monthly returns (1.32%), December gives investors the fewest loss-harvesting opportunities of any calendar month period of the year on a statistical basis.

Another potential detriment to harvesting losses in December is that it’s easy to pivot from loss harvesting into loss realization. The practical reality is that many American investors may take the cash for Christmas or other year-end cash needs. So rather than rotating losses back into markets, the risk is to just bank the losses. The result of this is that the investor’s allocation changes in a disjointed and unsystematic way and that the investor will not recoup their original value or gain any actual appreciation.

To state the obvious, investors are rooting for their holdings to increase in value over time. That’s the whole point of investing! But when markets are appreciating, rebalancing portfolios to maintain strategic allocation targets can often mean trimming the biggest winners and adding to relative laggards. While we remain diligent around tax implications when performing portfolio rebalancing, realizing some capital gains to maintain appropriate market exposure or to raise cash for portfolio distributions is inherently part of the game. By consistently looking for opportunities to harvest losses throughout the year, the overall tax friction of those practical realities can be partially offset by prudent tax loss harvesting consistently rather than as an event.

Ultimately the purpose of tax-loss harvesting, or what we might consider success in managing taxes along with market risk, means that depending on the circumstances, we may redefine success as reducing the tax cost of public market investing (as opposed to creating a net loss to stockpile for some eventual value realizing event like the sale of a business, real estate or other appreciated illiquid assets). In summary, there are plenty of good reasons to encourage investors to abandon the notion that tax-loss harvesting is an event to be considered once a year in the late fourth quarter.

2 https://www.forbes.com/sites/simonmoore/2018/11/08/why-you-should-tax-loss-harvest-now/#55e913067676

This material and the opinions voiced are for general information only and are not intended to provide specific advice or recommendations for any individual or entity. To determine what is appropriate for you, please contact your personal advisors. Information obtained from third-party sources are believed to be reliable but not guaranteed. The tax and legal references attached herein are designed to provide accurate and authoritative information with regard to the subject matter covered and are provided with the understanding that MBL Advisors Inc., is not engaged in rendering tax, legal, or actuarial services. If tax, legal, or actuarial advice is required, you should consult your accountant, attorney, or actuary. MBL Advisors Inc., does not replace those advisors. The use of trusts involves a complex web of tax rules and regulations. You should consider the counsel of an experienced estate planning professional before implementing such strategies.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. For important information related to MBL Wealth, LLC, refer to the Client Relationship Summary (Form CRS) by navigating to http://mbl-advisors.com. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. For important information related to M Holdings Securities, Inc, refer to the Client Relationship Summary (Form CRS) by navigating to https://mfin.com/m-securities. Insurance solutions are offered through MBL Advisors Inc.