Brian Gift, CFA — Chief Investment Officer — 704-335-4518

Capital markets seem to have become increasingly dynamic as the pace of innovation has compounded around the world, which in turn has given investors an endless list of variables to consider when constructing portfolios.

In this Investment Strategy Outlook, we will elaborate on various topics including investor sentiment, elevated valuations, diversification versus concentration within portfolios, inflation, interest rates, Trump, and AI.

In the end, we believe many of these factors will lead to the continuation of higher levels of nominal growth, interest rates and an ensuing extension of the profit cycle for corporate America. There will surely be plenty of surprises unanticipated by the countless 2025 “Year Ahead” outlooks written over the last couple of months. However, it seems that policy makers will be an obvious source of volatility (in both directions) for all asset classes in the year ahead.

Risk assets have demonstrated unease with 10-year bond yields above 4.5% +/- on numerous occasions over the last couple of years. A couple of large Wall Street Investment houses are putting 40% odds on the Fed having to reverse course and hike rates in 2025 (we disagree, but who knows for sure). America is far more sensitive to higher prices than we were prior to COVID, which in turn means that the bond market will demand that the Fed continues to thread the proverbial needle in balancing their dual mandate. Similarly, Trump was anything but a fiscal hawk during his first term as President, and 6% +/- budget deficits will likely not be tolerated by the markets indefinitely.

The bottom line is that the bond market will continue to have a significant influence on how most asset classes behave. Like many investors, we are rooting for a broadening of both fundamentals and performance beyond Mega Cap tech (“US exceptionalism”). We are optimistic that conditions are in place to support this narrative in the years ahead.

Investors are far more enthusiastic entering 2025 than they were to start 2023 or 2024, which seems to be well justified in many regards as economic data continue to track at a respectable level (Atlanta Fed GDPNow tracking at 2.3% for Q4 2024), the unemployment rate continues to hold steady near multi decade lows, credit spreads remain pinned to their cycle lows, and most importantly, earnings growth is forecasted to be robust for the foreseeable future.

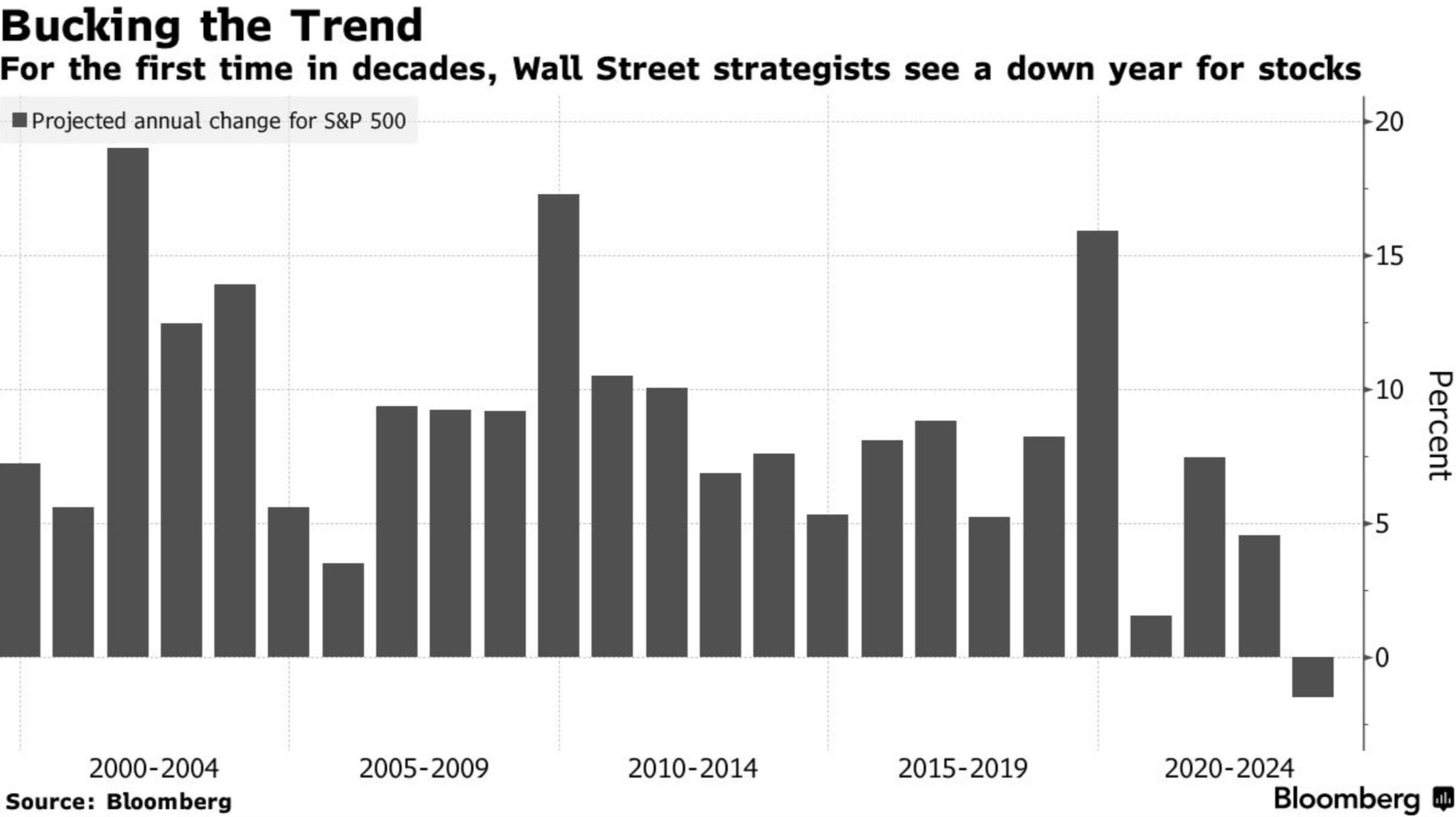

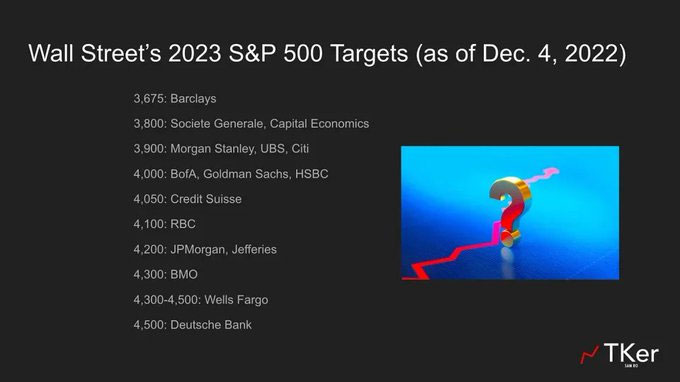

The majority of Wall Street strategists have set their S&P 500 price targets to forecast gains in the 10% – 15% range for 2025. This is a notable shift from 2023, when the average strategist price target projected a negative year (the only time this has happened since 1999. Source: Bloomberg). At the beginning of 2024, the outlook among strategists wasn’t much more bullish, as the average price target was only 2% – 3% above where the year began.

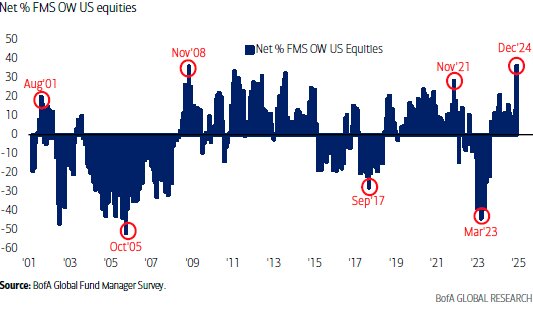

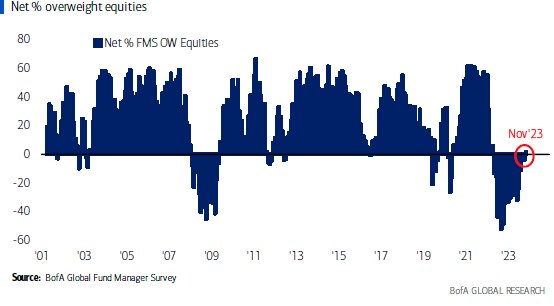

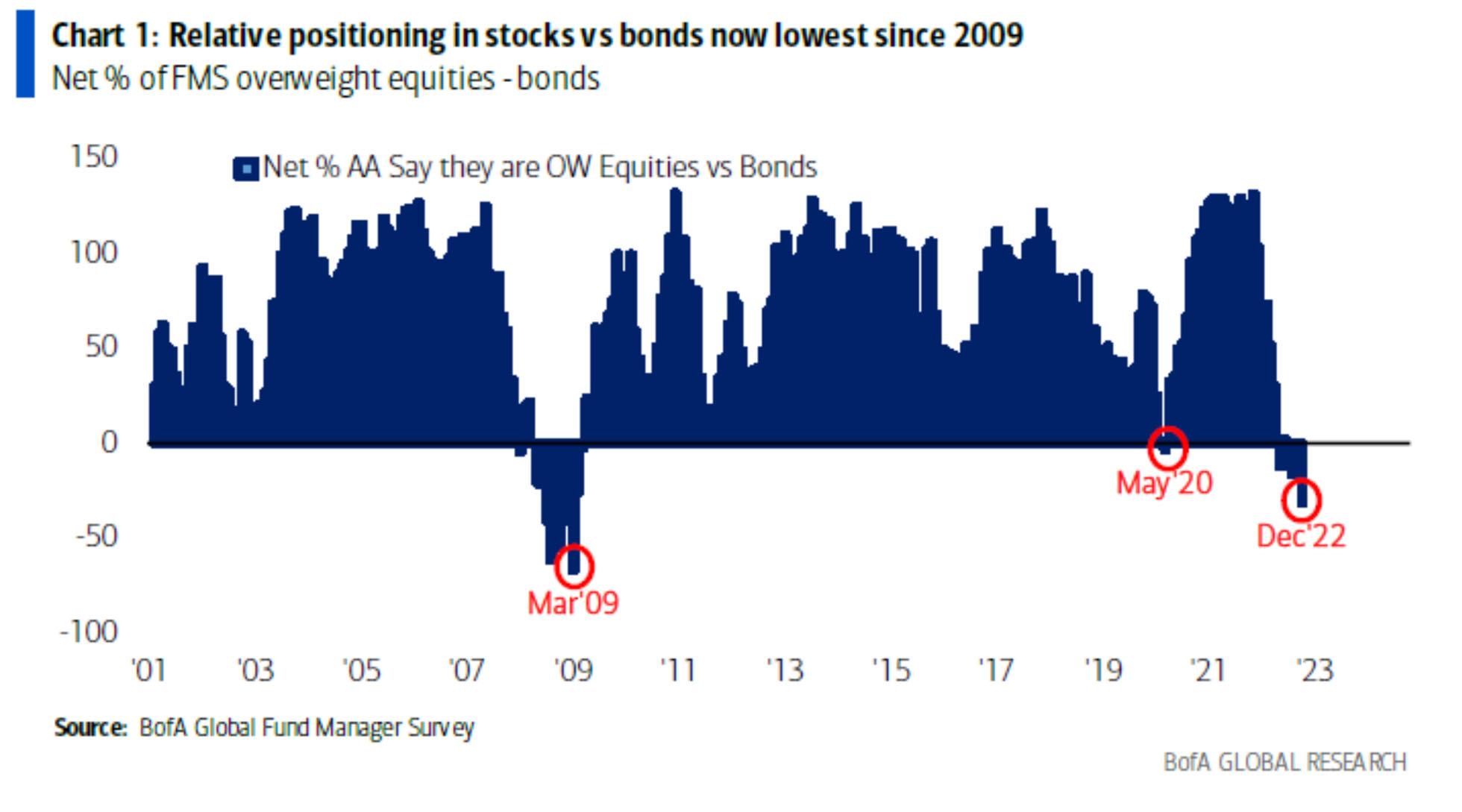

The Bank of America Global Fund Manager Survey is often a good indicator of how the consensus is positioned. In December 2024, the Fund Manager Survey showed a record overweight to US equities in the history of this survey going back to 1999. This is in comparison to March 2023 (SVB Bank failure), when investors were holding their largest underweight to US equities since prior to 2008.

Source: BofA Global Research

The December Fund Manager Survey also revealed a similar dynamic with broad equity positioning relative to cash. Today, equity positioning is near its previous peaks relative to cash. It’s worth noting that the inverse was true in September 2022, precisely when the previous bear market ended, and investors held an all-time underweight to stocks vs. cash.

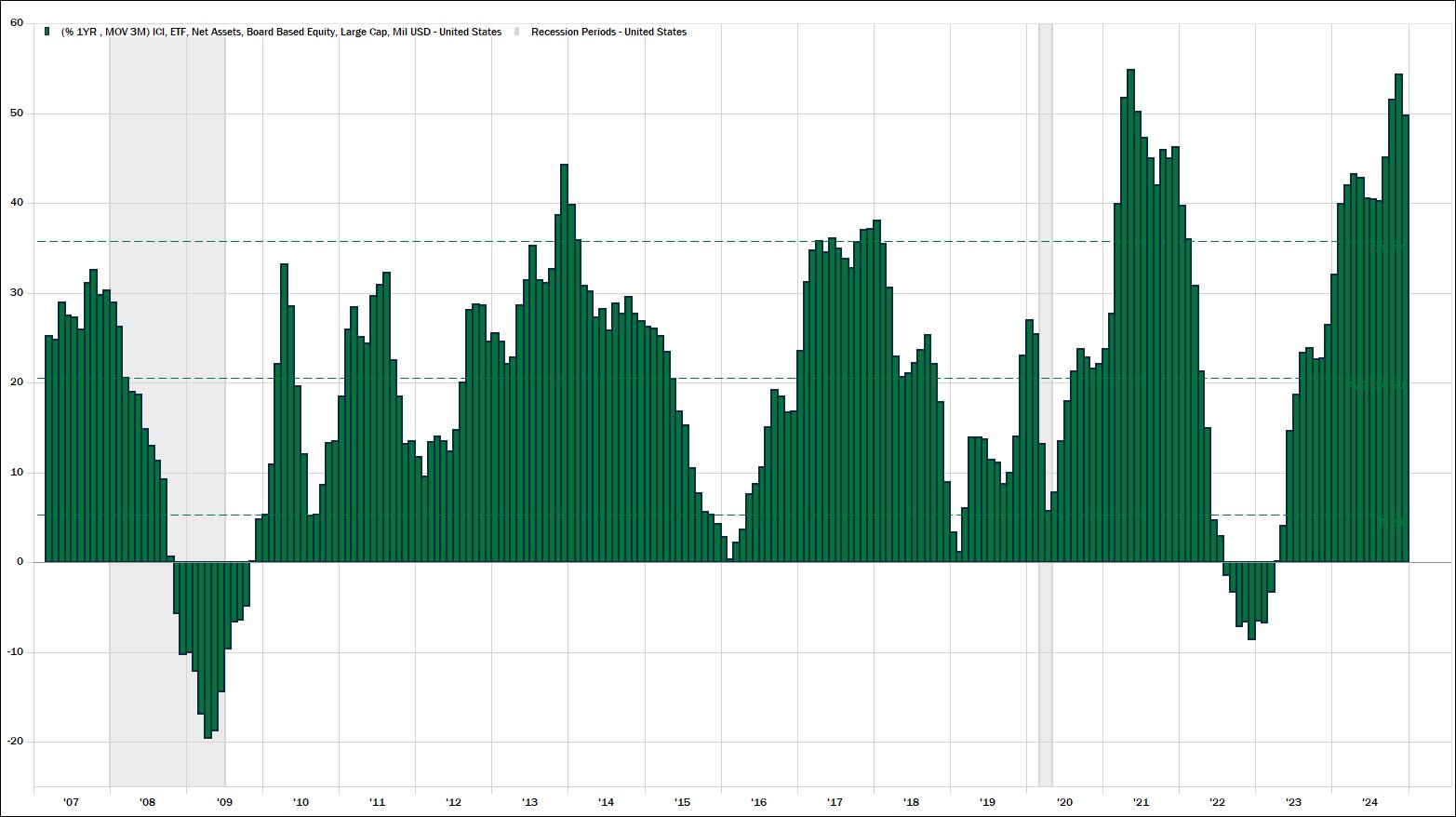

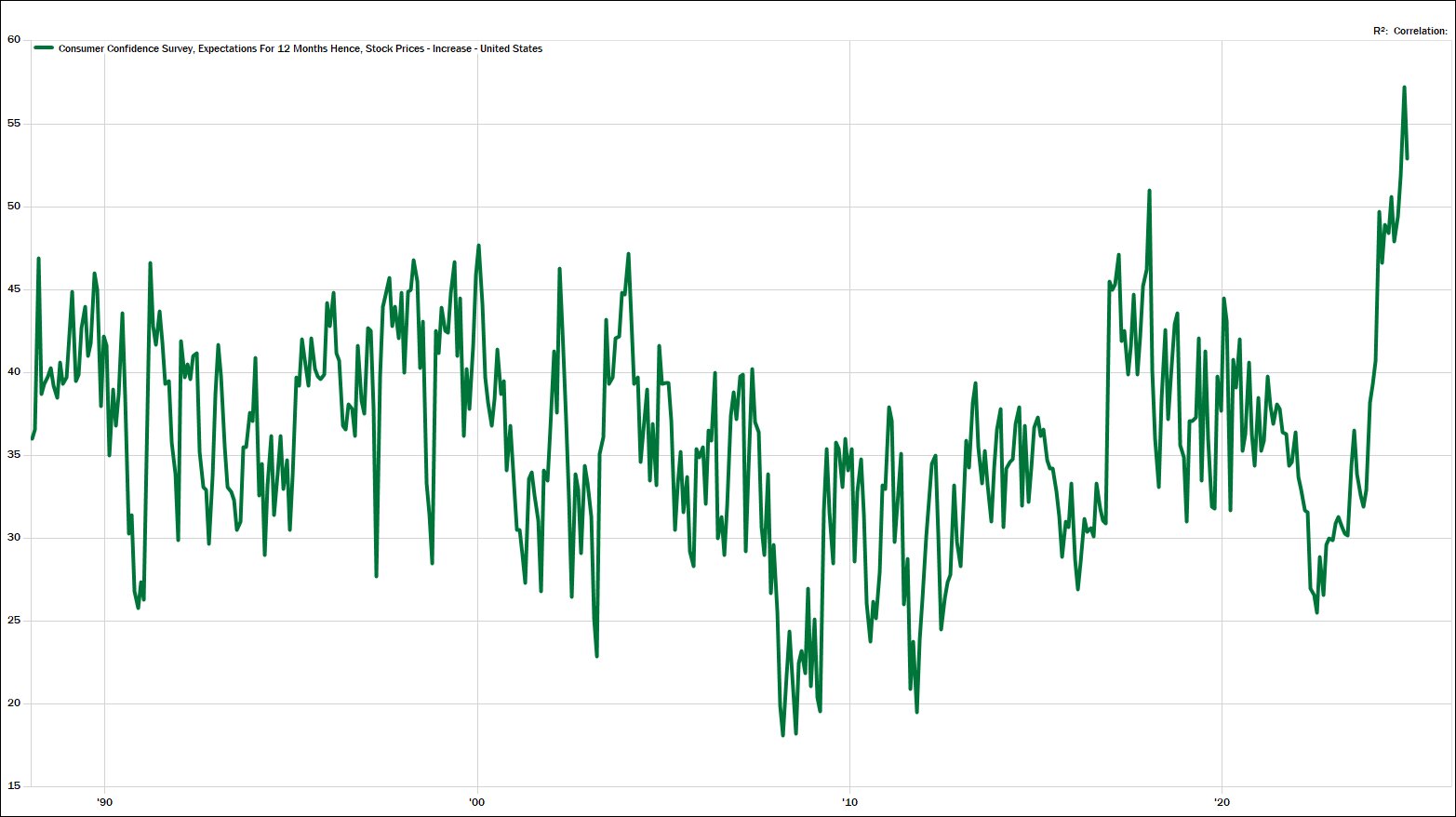

Myriad additional data points corroborate this same message. A few others of note are:

Source: MBL Advisors & FactSet

Source: MBL Advisors & FactSet

Much of this is the natural course of evolution during a bull market. In isolation, none of these data points tend to signal the end of a bull market. But they could offer a clue suggesting that investors may need to wrestle with their own (lofty) expectations at some point in the year to come.

Economic weakness and an ensuing recession are no longer perceived as the primary danger to asset prices by most investors, contrary to a large swath of the past three years. Goldman Sachs recently noted: “80% of our clients expect US GDP to grow above 2% this year and no one anticipates a recession, with only 1% of clients expecting US GDP growth below 1%. This is in stark contrast to 2024 and 2023, when 27% and 57% of people, respectively, expected a recession” (source: @zerohedge).

Even David Rosenberg, the famed market bear, and incredibly astute research analyst, issued an apology to investors last December in his note titled “Lament of a Bear” (source: @EconguyRosie). This followed some of his less than optimistic counterparts losing their jobs earlier in the year (Chief Strategists at JP Morgan & Morgan Stanley).

Despite the bears on Wall Street becoming an increasingly rare breed, the media is eager to remind us of the plethora of potential worries: tariffs, inflation, weak growth outside of the US, higher interest rates, a strong USD, fiscal excesses, a Fed policy error, other things that go bump in the night. But investors are often well served in remembering that bull markets usually climb the proverbial “wall of worry.” Markets often get into trouble when signs of discomfort have largely disappeared (2018, 2021, etc.).

When putting macro / headline risks to the side for a moment, we do believe that there are two hazards which are potentially underappreciated by investors today. First, nearly all fundamental valuation metrics are registering in the 90th to 99th percentile of historical data (2009 was the exact opposite). And second, index concentration has reached multi-decade highs for the S&P 500. This is not to say that there is a shortage of attention on either of these issues, but some investors seem to expect these trends to continue almost indefinitely.

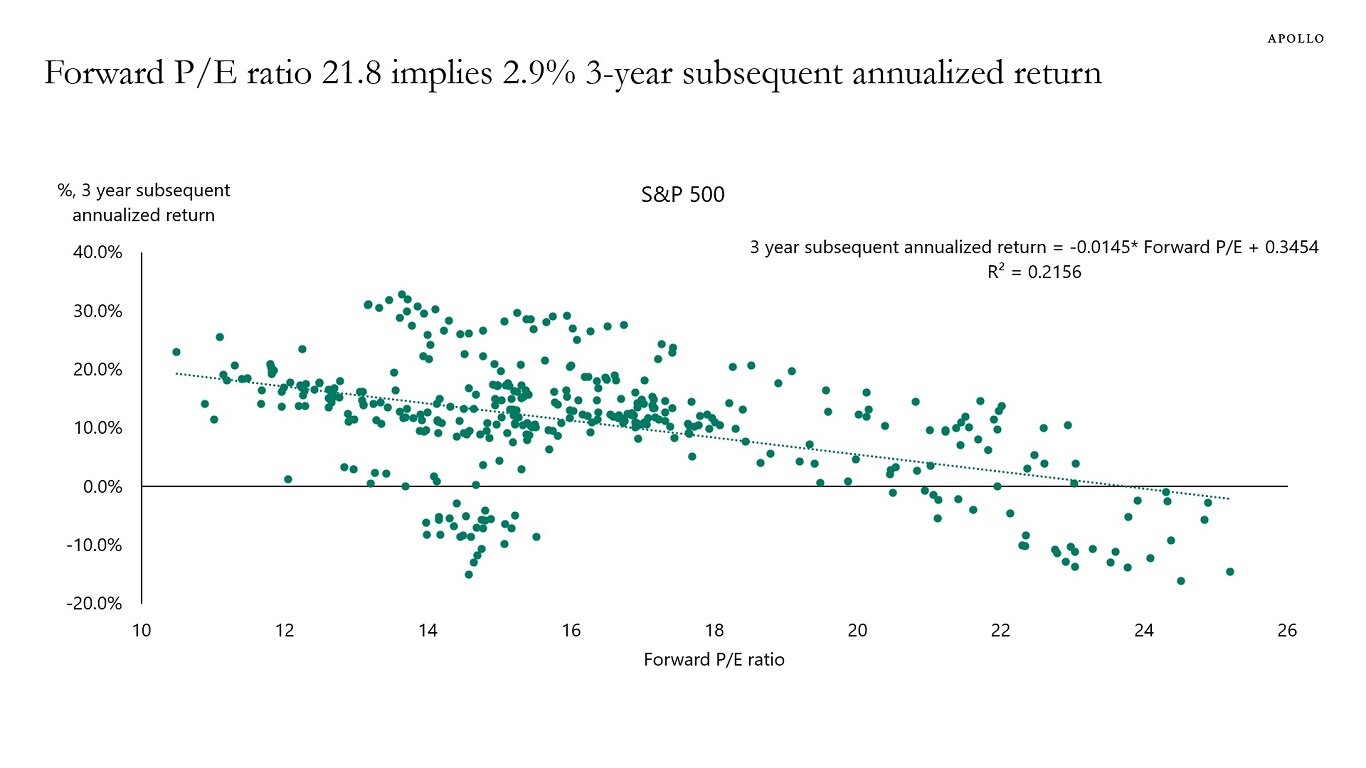

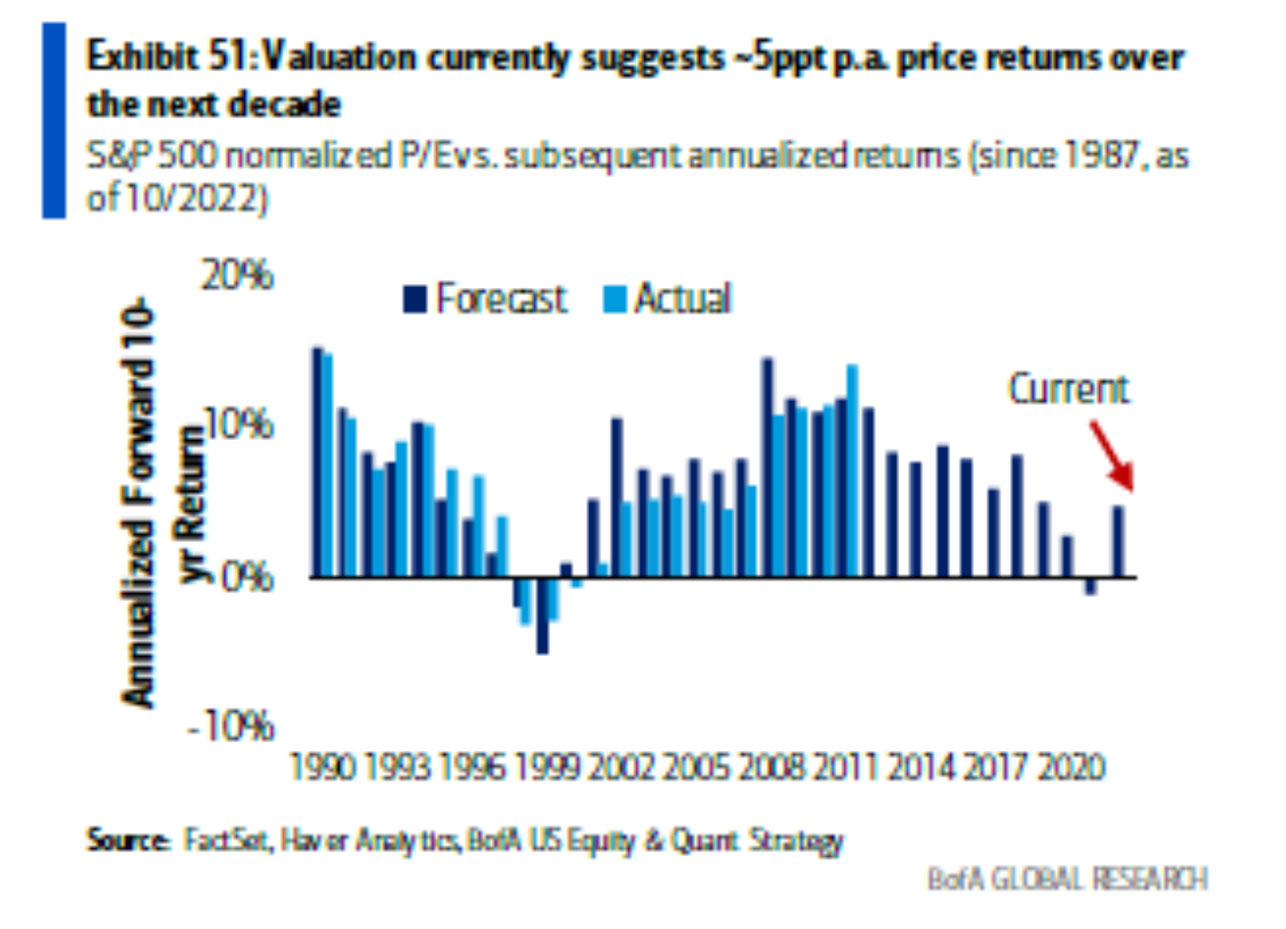

Last October, Goldman Sachs, Apollo and Bank of America Global Research simultaneously noted that they expect the S&P 500 to compound at roughly 3% per year for the next several years (+/- a few % on either side). More recently, Morningstar has joined this crowd. Apollo is relatively more bullish compared to the others, as their 3% return forecast “only” lasts for three years. Bank of America Global Research and Goldman Sachs projected 3%+/- returns for the next decade, given where starting valuations are today.

Source: Apollo & Torsten Slok

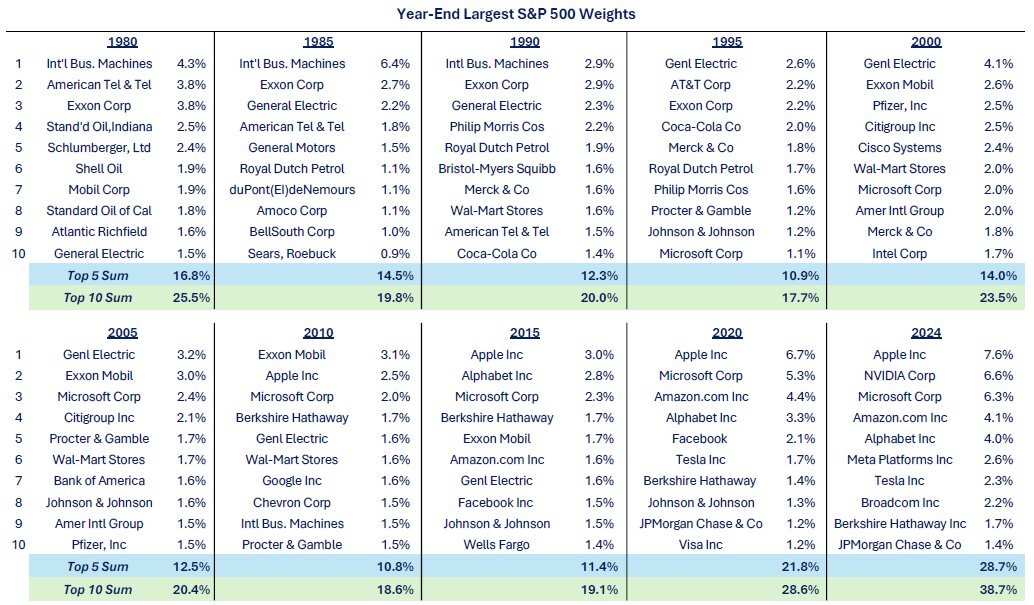

The historically elevated valuations in US Large Cap equity indices are directly tied to the increased concentration within these indices themselves. The largest 10 stocks are some of the most expensive stocks in the market from a fundamental standpoint and now make up 39% of the S&P 500. The top five names account for 29% of the index. We haven’t seen these levels of concentration within the S&P 500 in nearly 70 years. For most of the last 40 years the top 10 stocks constituted roughly 20% +/- of the index, while the top five names made up 11% – 15% of the S&P 500. Thus, the concentration of the top five and top 10 names in the index has effectively doubled relative to most of the last 50 plus years.

This has served investors well for the last decade as the largest names have also been the best performing names during this time. This has made the S&P 500 virtually an unbeatable index for investors who have higher levels of diversification within their portfolios.

The cap weighted S&P 500 roughly doubled the performance of the equal weighted S&P 500 in 2023 and again in 2024. The reason for this can be simply explained in the fact that the largest 10 names accounted for 68% of the index’s total performance in each of the last two years (source: Strategas Research Partners). Carter Braxton Worth of Worth Charting noted that “2024 was a not so spectacular year for US equities. The Russell 3000 (98% of the investible US Equity Market) was +22%, yes, but the median performance of the Index’s constituents was 3.82%. 1331 stocks in the index were DOWN (45.7%). Sobering” (source: @CarterBWorth).

It is important to note that valuations are a terrible timing tool and offer no predictive power over shorter time frames. This is especially true when animal spirits are running hot as they seem to be today. However, the simple average trailing twelve-month PE ratio (i.e. based on 2024 EPS) for the 10 largest stocks in the S&P 500 currently stands at 46x (source: MBL Advisors & FactSet 1/30/25).

Source: Todd Sohn, CMT & Strategas Research Partners

Aside from the early 1970’s, the late 1990’s and the 2020’s, the equal weighted S&P 500 has outperformed the capitalization weighted S&P 500 throughout most intermediate to longer term time periods over the last several decades. One big question for investors is whether the dominance of the largest stocks in the market is the “new normal” or if dramatic mean reversion lies ahead? Eventually, we believe the beneficiaries of AI will expand well beyond the Mag 7, and this will serve as a catalyst for some mean reversion in market performance.

Savita Subramanian and Bank of America Global Research are firmly in the mean reversion camp as their 10-year forecast is far more bullish for the equal weighted S&P 500. Savita believes that the equal weighted S&P 500 could compound at roughly 8% +/- per year for the next decade if dividend payout ratios mean revert higher back to their long-term averages. Richard Bernstein of RBA Advisors was Savita’s mentor at Merrill Lynch a few decades ago, and he also shares a similar opinion.

We believe that the increasingly popular analogies to the tech bubble are a poor comparison to the current market environment. The best performing stocks of the last few years are some of the highest quality businesses in the history of corporate America, which is much different than the TMT bubble. However, the Nifty Fifty environment from the 1970’s may offer some parallels, when investors bid up the largest stocks in the market to unsustainable valuations and considered most other businesses not to be worthy of their capital.

Ed Yardeni (Yardeni Research) and Tom Lee (FSInsights) continue to be two of the most optimistic strategists on Wall Street. They also happen to be two of the most accurate strategists of whom we are aware, over the last 15 years. Yardeni believes the S&P 500 will finish this decade around 10,000 as earnings for the index will be roughly $400 per share. If 2025 and 2026 earnings stay on track with current estimates, Yardeni’s earnings forecast could become increasingly consensus as time passes.

Tom Lee (FSInsights) has published some even more bullish scenarios than Yardeni. Lee believes that meaningful bear markets often coincide with generations moving beyond peak spending years (28-48 years old). Millennials have another decade plus of peak spending ahead of them, which Tom believes is a positive catalyst for US equities, all else equal.

Source: FSInsights & Tom Lee

Both of these strategists believe we are in the middle of a technology driven productivity boom. And if this continues, historically high corporate operating margins will hold steady, and therefore support earnings in the years to come. In their opinion, more profitable businesses which also exhibit secular growth characteristics (Mega Cap Tech) are largely deserving of elevated valuations relative to historical “norms.”

In his 2025 technical outlook, Stephen Suttmeier from BofA Global Research published the following:

“In 2025 the SPX will enter the 12th year of its secular bull market. The secular bull markets from 1950 – 1966 and 1980 – 2000 lasted 16 and 20 years respectively, which means the current secular bull market is mid to late cycle and can extend until 2029 to 2033… The SPX looks overextended on its move to 6000 in late 2024. This roadmap chart shows SPX achieving 6000 in mid-2026, not late 2024 and suggests that 2025 could see downward mean reversion.”

Regardless of how 2025 plays out, it should be noted that comparison to these previous secular bull market roadmaps project meaningful upside for the S&P 500 before this secular bull market is finished.

Brian Belski, the Chief Investment Strategist at BMO Capital Markets, believes we are returning to a “normal” environment for both the economy and capital markets alike. His definition of “normal” refers to the investment environment prior to 2008. The post GFC environment has been abnormal in many regards, as central banks and governments around the world have become fond of enacting various measures of fiscal and monetary policy which are unconventional and extreme by historical standards. Jason Trennert of Strategas Research Partners recently wrote “Reversion to the mean, at least until the introduction of extraordinary monetary policy, had been one of the most reliable concepts in finance, if not life itself.”

The most important asset price in the world, the US 10 Year Treasury Bond has certainly normalized to a large degree. 10-year bond yields approaching 5% seem high to many investors relative to fifteen years of artificially low rates. But going back to 1950, the average yield on the 10 Year Treasury is 5.62% and the median yield on the 10 Year Treasury bond is 4.96% (source: MBL Advisors & FactSet).

Despite conventional thinking, higher bond yields are not necessarily a bad thing, if they are associated with stronger economic growth. Real GDP was below 2% for the entire period between 2008 and COVID. For the last few years, the US economy has surprised to the upside with 2% – 3% Real GDP growth, thanks to higher levels of productivity (and government spending), coupled with 5% – 6%+ nominal GDP growth. These levels of growth were declared a thing of the past by many economists during the post-GFC era.

Higher levels of nominal GDP are favorable for corporate profitability since revenues grow in nominal terms. In this regard, Belski believes that companies can grow earnings, across a plethora of industries and market caps, by upper single digits rates in the years to come. He also believes that US equity markets should compound at a similar rate over the next three to five years.

Mega Cap Technology (related) companies have carried the earnings growth for the entire market for the last two years. These businesses are expected to grow earnings at a very healthy rate again in 2025, but earnings momentum is projected to slow relative to the last several quarters. Conversely, earnings momentum is expected to accelerate across most other parts of the market (sectors and sizes) in 2025. This will be a “show me” story since investors have been waiting for this narrative to come to fruition for several quarters now. Nonetheless, if corporate America (excluding Mag 7) can deliver on the expectations for solid earnings growth, this should be an incredibly welcomed and positive catalyst for investors in 2025.

Source: JP Morgan Guide to the Markets

Further supporting the potential dynamic for a broadening out of leadership beyond the largest market capitalization names is the following analysis from John Roque, Chief Technical Strategist at 22V Research:

Dennis DeBusschere of 22V Research stated that “Small Caps have dramatically under-earned nominal growth. That is expected to revert in 2025. There is little reason to fade that outlook. This is a large part of the reason we favor small caps in 2025.”

To be clear, we favor US Mid Cap stocks over US Small Cap stocks. US Small Cap stocks have their issues, as roughly 40% of the Russell 2000 index is non-profitable and these businesses are usually more sensitive to higher interest rates. At the same time, smaller businesses could be the disproportionate beneficiaries from deregulation, and the NFIB Small Business Optimism Index has surged since the election.

In the January 2025 BofA Global Fund Manager Survey, Michael Hartnett’s “Bottom Line” was that “investors are bullish the US$ & (US) equities, bearish everything else.” Chris Verrone of Strategas Research Partners often notes that the golden rule of this business is that “sentiment follows price.” Bonds, cash, and equities outside of the United States have not given investors many reasons to be bullish over the last few years.

MBL Advisors remains meaningfully underweight non-US equities relative to our strategic targets, as we have for nearly the entirety of the last seven years. Taking a contrarian stance simply for the sake of being contrarian is rarely a good strategy in isolation. Having said this, some interesting setups may be taking shape in equity asset classes other than US equities.

European equities are trading at their largest discount ever to US equities on a forward PE basis (Source: Strategas Research Partners). Part of this dynamic is due to the premium valuations which US technology stocks are awarded by investors, and the lack of similar businesses which exist within the European indices. However, this historically high valuation premium persists when neutralizing the sector exposure between the two indices. It is also important to mention that the Euro Stoxx 600 is at all-time highs, in local currency terms. Thus, this valuation gap does not exist solely due to poor absolute performance from European equities.

President Trump recently mentioned he believed that 600,000 – 700,000 Ukrainian soldiers had been killed in the Russia – Ukraine war. He also said that Russia had lost 800,000 soldiers. These figures are 10x – 15x higher than what is being reported by Russia and Ukraine themselves. Surely Trump can exaggerate at times, but these statistics are likely more directionally accurate than the drastically lower figures Russian and Ukraine are citing. Regardless, Trump is beginning to speak about using sanctions as a tool to incentivize an end to the fighting. All else equal, European equities might demand less geopolitical risk premium if some sort of resolution is reached between Russia and Ukraine in the months ahead. The December 2024 BofA Global Fund Manager Survey noted that investors have a near record overweight to US equities relative to Eurozone equities, going back to 2001.

Chinese equities are the ultimate wild card as we enter 2025. China’s economy is nothing short of a disaster, as they are in the middle of a deflationary debt spiral, best observed through the tanking of their bond yields and their slowly weakening currency. Their one child policy of the last few decades has created a demographic time bomb, and the trick seems to be up on the centrally planned investment spending which helped catalyze their economic boom years of the past. Currently, Beijing is striving to stimulate the consumer through various measures as their economy continues to slow, and they wait to find out the extent to which increased tariffs will impact their economy. The size and scope of their stimulus response will likely be directly tied to the enviable tariff policies coming from the new administration.

We don’t pretend to have any edge in investing in China, and less than 1% of our portfolios have exposure to their equity markets. Having said this, the two best technical analysts of whom we are aware of, Jeff deGraff of Renaissance Macro and Chris Verrone of Strategas Research Partners, are both bullish on Chinese equities as we enter 2025 (shockingly, Chinese equities outperformed US equities in 2024). They believe we encountered some very rare and bullish signals in the Chinese equity markets last fall when their stimulus program was originally announced and Chinese equity markets rocketed higher for a few weeks. Cyclical sectors have continued to exhibit strong relative performance versus defensive sectors since then, while fund flows and sentiment have once again turned (contrarian) bearish (source: Jeff deGraff & Renaissance Macro).

When extending our time horizon beyond the next few months, and possibly even the next few years, it is interesting to think about the following: The United States is 4% of the global population, 25% of global GDP, 55% of global profits and near 70% of the global equity market capitalization. The US made up roughly 50% of the global equity market capitalization a decade ago. How much further can these dynamics stretch?

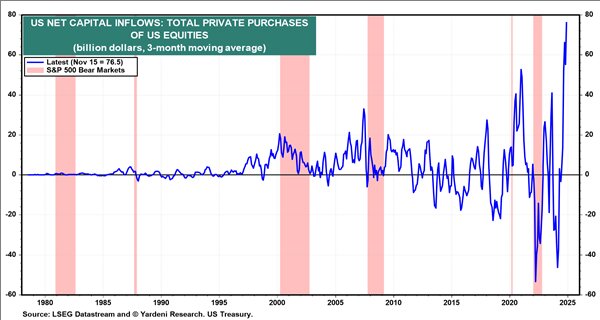

Even non-US investors have flocked to US equity markets recently. Ed Yardeni recently noted that “over the past three months, foreigners purchased US equities at a record pace of $76.5 billion. One note of caution: Their buying has a record of being a contrary indicator. They tend to be big buyers right before bear markets” (source @neilksethi).

Source: Yardeni Research

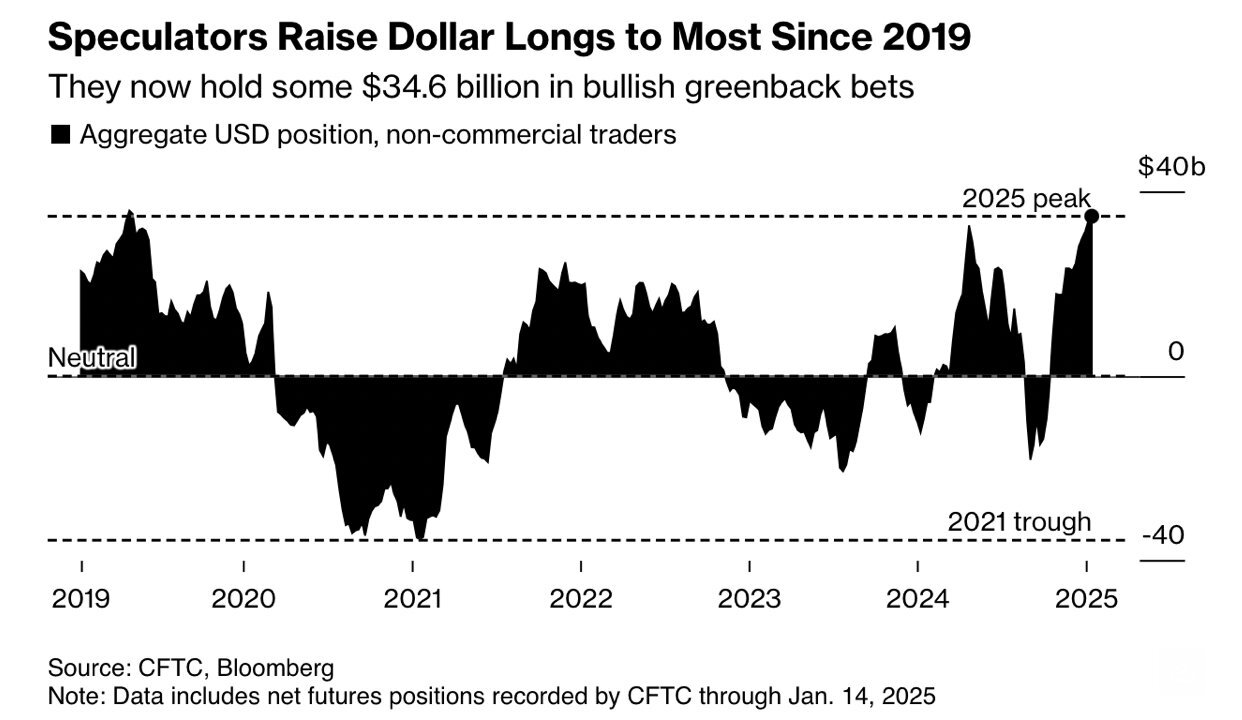

The strong US dollar has been a headwind for US investors investing capital outside of the US for over a decade. And the move higher in the USD index since the election has been pronounced. The Trump Administration’s “America First” policies, tariffs, US Tech exceptionalism, stronger growth in the US relative to the rest of the world, and higher interest rates in the US versus virtually all other developed countries are all supportive of the greenback.

Given all of these “obvious” factors, most investors are heavily positioned for further strength in the US dollar. And every time Trump opens his mouth about Tariffs the US dollar moves higher. However, an unexpected catalyst, such as a couple of relatively benign inflation readings or global growth improving relative to the US, could cause a rapid unwind of this trade. “The US dollar is trading 23% above fair value, the largest divergence on record”, according to BofA Global Research (source: @kobeissiLetter). Equity markets will likely display an increased sensitivity to moves in bond yields and exchange rates than they have at various times over the last year.

Source: Bloomberg

Finally, it was not long ago that investors dreamt of being able to achieve 4.5% – 6% yields from high quality investment grade fixed income. Although this is the reality today, many investors seem uninterested in deploying capital into this asset class. The poor performance investors have experienced in fixed income investments over recent years is undoubtedly a significant factor influencing their negative sentiment towards bonds. Jim Bianco of Bianco Research pointed out that the rolling three-year return from US Long Term Bonds is the worst stretch in 180 years.

One of the great underpinnings to the 2009 – 2021 equity bull market was the fact that stocks were fundamentally attractive relative to the historically low bond yields we experienced during that time frame. Now that bond yields have normalized, while equity valuations have continued to drift higher, the Equity Risk Premium for the S&P 500 is below 0, for the first time since the tech bubble (source: MBL Advisors & FactSet).

Theoretically, the Equity Risk Premium is the excess return investors should expect to hold (volatile) equities, over 10-year US Treasury Bonds. This metric now states that investors are no longer being compensated to own large cap equity indices, as they can earn a similar return by holding nearly risk free 10 Year Treasury Bonds.

Having said this, we believe the Equity Risk Premium is a somewhat flawed metric in the sense that bonds don’t have two important traits which US Large Cap equities exhibit in a meaningful way. First, equities are a real asset, and thus a good hedge against inflation, over longer time frames. If inflation and nominal growth have a higher resting heartbeat, as they have since COVID, this metric could be overstating the attractiveness of bonds relative to stocks. Second, the S&P 500 has an increasing amount of exposure to “innovation”, which is a primary source of the currently high valuations, while fixed income clearly has no upside optionality.

As we have stated in the past, we are grateful not to have to play the thankless game of publishing S&P 500 targets. Charlie Biello of Creative Planning noted that PE multiples expand or contract by at least 10% in 70% of calendar years. Outside of major economic turning points, Wall Street is fairly good at forecasting earnings estimates for corporate America. However, forecasting valuations for the market has been nearly impossible, especially during this era of excess liquidity. Nobody believed the S&P 500 would trade back to multiples we witnessed during the COVID mini bubble, but that is precisely what happened in 2024 for US Large Cap equities.

Entering 2025, most strategists are extrapolating the S&P 500 trading at 22x forward earnings as the “new normal” at least for the time being. However, history says investors should bet on the S&P 500 trading either above 24x NTM EPS (this seems very difficult to imagine, but so did getting to these valuations in the first place) or below 20x NTM EPS by the end of this year. Holding 2026 earnings growth steady at today’s forecast, this would mean that there is a 70% probability that the S&P 500 finishes 2025 either below 6000 or above 7200. Of course, most strategists’ forecasts squarely between these two bookends. This serves as a good reminder that the stock market is far more volatile than its underlying fundamentals.

| Statistic | Average % Return the Following Year | % of Positive Years | Sample size | Data Since | Source |

|---|---|---|---|---|---|

| The S&P 500 does not close below its 200 Day Moving Average in a given calendar year (2024) | 4.62% | 55.00% | 11 | 1950 | Bespoke Research |

| Year 3 of a Bull Market (Nov 2024 – Nov 2025) | 4.80% | 67.00% | 12 | 1932 | Strategas Research Partners |

| Year after two Positive Years in a row | 5.20% | 67% | 18 | 1936 | BofA Global Research Stephen Suttmeier |

| Decennial Cycle Year 5 | 20.70% | 92% | 14 | 1885 | NDR Research |

| Stock Performance after Years with over 50 Record Highs (2024) | -3.00% | 28% | 7 | 1928 | NDR Research |

| Year 1 of Presidential Cycle (2025) | 6.60% | 58% | 14 | 1928 | BofA Global Research Stephen Suttmeier |

| Positive January in Year 1 of Presidential Cycle (2025) | 13.90% | 79% | 14 | 1928 | BofA Global Research Stephen Suttmeier |

| Presidential Cycle Year 1 (2025) following up years in both Year 3 (2023) & Year 4 (2024) | 1.90% | 63% | 8 | 1936 | BofA Global Research Stephen Suttmeier |

| 4 Straight days with more than 70% of S&P 500 stocks advancing (1/19/25) | 10.63% | 92% | 12 | 1990 | Seth Golden |

| S&P 500 has at least 4 losses > -1% in days within 30 days of a Record high (January 2025) | 9.90% | 70% | 20 | 1928 | Sentiment Trader |

As inflation fears creep back into the headlines, criticizing the Fed for being too Dovish has become popular again, although it was only four short months ago when many of these same prognosticators believed the economy was weakening and the Fed was too tight. The Fed began their cutting cycle in September 2024 by reducing the Federal Funds rate by 50 basis points. Since then, they have made two additional 25 basis points cuts to their policy rate. The unique thing about this cutting cycle is that the 10 Year Treasury yields have increased by roughly 1% since the Fed began their cutting cycle. A 200-basis point steepening between the Federal Funds Rate and the 10-year Treasury, four months into a cutting cycle, is unprecedented.

Bond yields accelerated their assent higher when Federal Reserve Chairman Powell mentioned that their “inflation forecasts have kind of fallen apart” in his press conference after the December FOMC meeting. In addition, the minutes from the December FOMC meeting show that most voting members believe that inflation risks are to the “upside” relative to the FOMC’s base case forecasts for inflation over the coming year. This is in stark contrast to the minutes from their September meeting when most FOMC members believed that inflation risks were “balanced” (source Neil Dutta & Renaissance Macro). Neil Dutta, Chief Economist at Renaissance Macro, pointed out that it is very clear what is occurring, which is the Fed is incorporating Trump’s tariff plans into their forecasts, despite Powell being adamant about the fact that they are strictly “data dependent.”

The trend for rising inflation forecasts has not slowed much in 2025, as the ISM prices paid by purchasing managers index (leading indicator for CPI) hit a 22-month high.

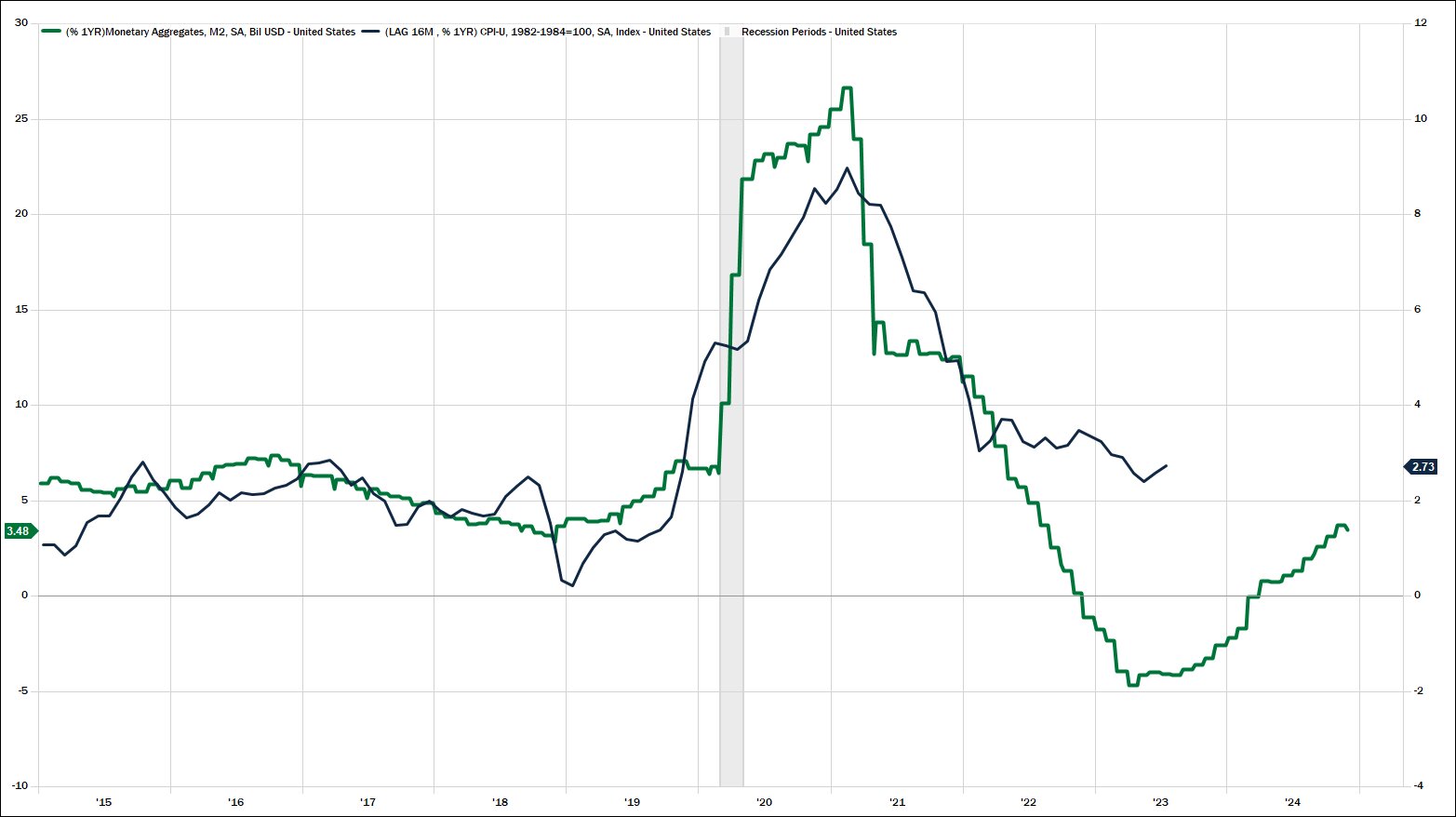

All of this is happening while the money supply (M2) is beginning to accelerate again. Possibly the greatest economist of all time, Milton Freedman, is famous for saying that “inflation is always and everywhere a monetary phenomenon.” This is to say, inflation is always as simple as an increased amount of dollars chasing the same amount of goods.

Source: MBL Advisors & FactSet

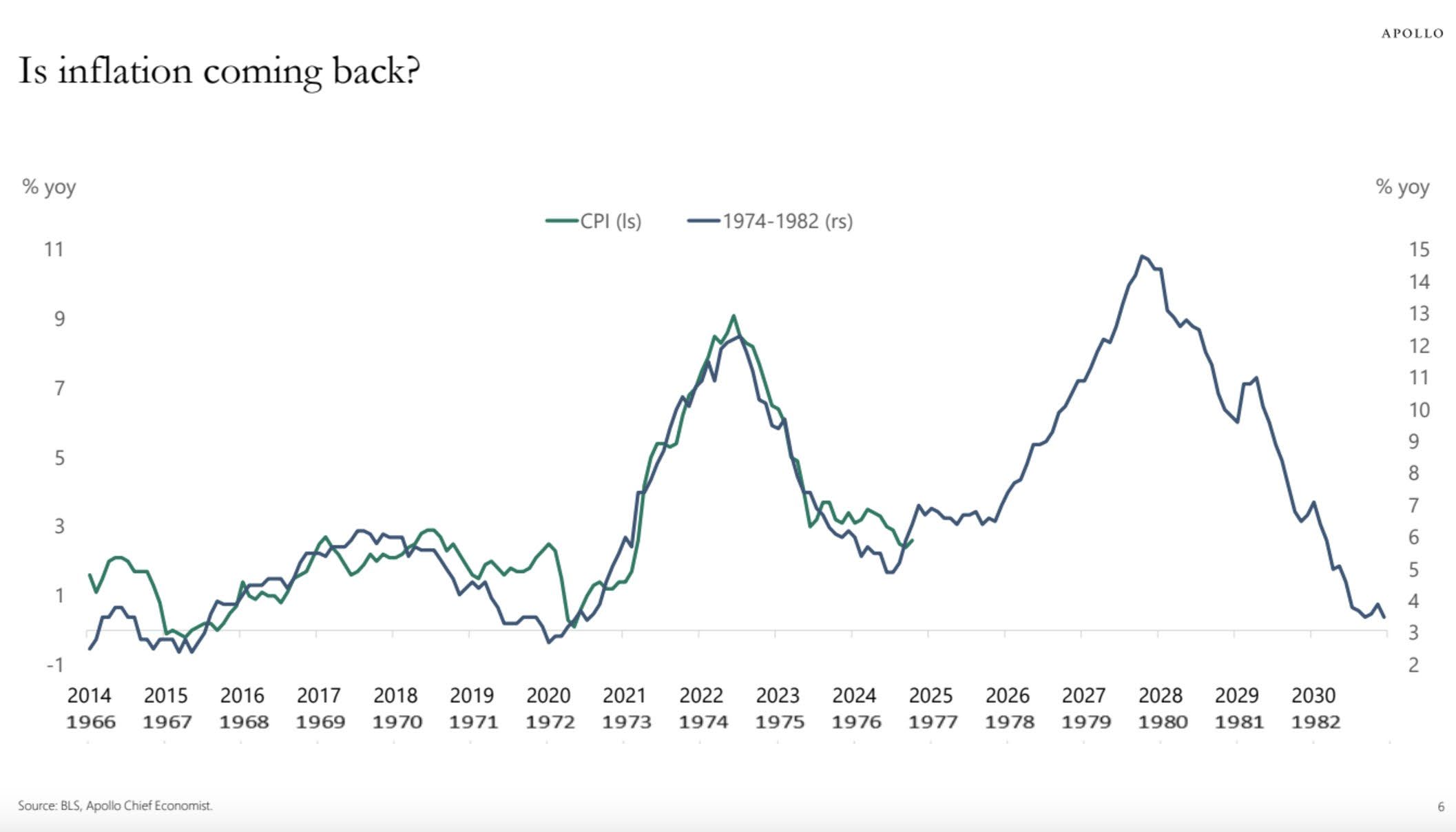

For two years, Don Rissmiller of Strategas Research Partners has been mentioning that there is an 87% chance for developed economies to have a second wave of inflation once a given economy experiences a first significant bout of it. The now famous chart below comparing the current path of inflation vs. the 1970’s (dual scale) shows that a second wave of inflation would begin in 2025 if the 1970’s roadmap was followed again.

Source: Apollo & Torsten Slok

Although we believe there is plenty of credence to the narrative that inflation will remain sticky and elevated above the Fed’s 2% stated target, we also believe the second wave of inflation thesis is overblown, at least for the next six to nine months.

Neil Dutta from Renaissance Macro believes the job market is showing some signs of softening underneath the surface. Not necessarily to problematic levels for the economy, as layoffs remain low, but the quits rate is down to 2.1%, the lowest level since April 2015 (excluding the spring of 2020). The quits rate is a terrific leading indicator for wage growth. Dutta stated that “the continued slide in the quits rate implies little need for firms to pay up workers; thus, I would anticipate continued slowing in compensation growth in the quarters ahead.” Dutta went on to mention that ISM prices paid reflect tariff fears, not underlying inflation, and new job postings remain weak.

Dutta is one of many economists who have noted that the housing market cannot handle 7% mortgage rates. Home building stocks are not trading well, as new home inventories continue to grow. This thesis was collaborated on January 23, 2025, when the BLS All tenant Rent Index, a leading indicator of shelter inflation, hit fresh cycle lows of 3.18%. Dutta went on to mention that the New Tenant Rent Index actually contracted by -2.4%. Dutta stated that the NTR is often directionally accurate but can overstate the degree of change at times. The bottom line is that if shelter inflation cools to the degree that Dutta and some other economists expect, there could be downside risks to inflation relative to consensus expectations in the months ahead.

Basic fixed income principles dictate that economic growth expectations and inflation expectations are the primary drivers of bond yields, aside from the very short end of the yield curve which the Fed controls.

Newfound beliefs regarding a resurgence of inflation have caused some investors to use the rise in bond yields to support their inflation claims. To be fair, 5-year breakeven rates are up more than 50 basis points since Fall 2024, but those were the cycle lows, and 5-year breakeven rates are hovering around 2.5% today, which seems like a very reasonable level of inflation expectations for the next several years.

In our opinion, the larger issue for bond yields is that investors are rightfully demanding an increased term premium to hold longer dated bonds given the higher levels of uncertainty associated with such maturities. In this regard, the abnormally flat yield curve we have witnessed for a large portion of the last 15 years was largely an anomaly, and a byproduct of hyperactive central bank intervention.

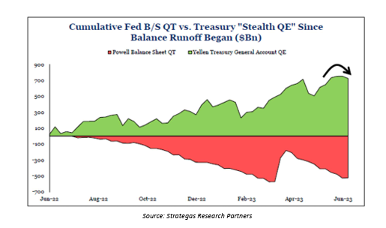

Jason Trennert from Strategas Research Partners recently wrote: “to the extent to which all Presidents, Democrat or Republican, grease the skids for their re-election, it was not particularly surprising that the Biden Administration used its powers to boost the economy and the financial markets. But the sheer range of tools used – the TGA, the SPR, student loan forgiveness, the Treasury Department’s suspension of the coupon issuance, not to mention a budget deficit of nearly 7% of GDP – was, indeed, breathtaking and unprecedented for an economy near full employment. With a debt ceiling debate looming and the Fed’s reverse repo facility falling to $240B from $2.5T at the start of 2023, there is a chance that the long-term interest rates could rise simply on the supply issuance alone. In short, the Trump Administration is inheriting an economic mess if it is serious about putting the country on a more sustainable fiscal path.”

An oversimplified rule of thumb is that 10-year Treasury yields should loosely track the rate of Nominal GDP growth over time. In this regard, 4.5% +/- 10-year bonds yields are not elevated, relative to the current growth rate of the economy.

We may have never publicly written about such a polarizing subject as President Trump. We recognize the people reading this will have wide ranging viewpoints regarding the President, and thus we will strive to remain as objective as possible. In this regard, we will begin with two important reminders:

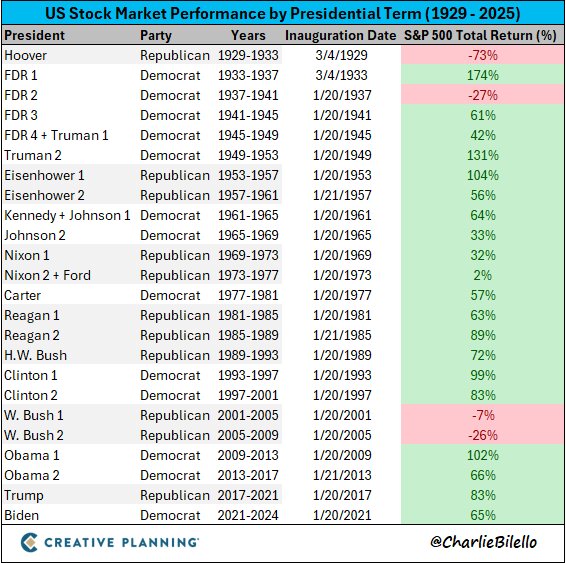

Stocks have done well regardless of who the President has been throughout history. The exceptions to this rule are Hoover & FDR during the Great Depression and George W. Bush, who began his presidency with the biggest asset bubble in the history of our country and ended with the largest financial crisis since the 1930’s.

Source: Charlie Bilello & Creative Planning

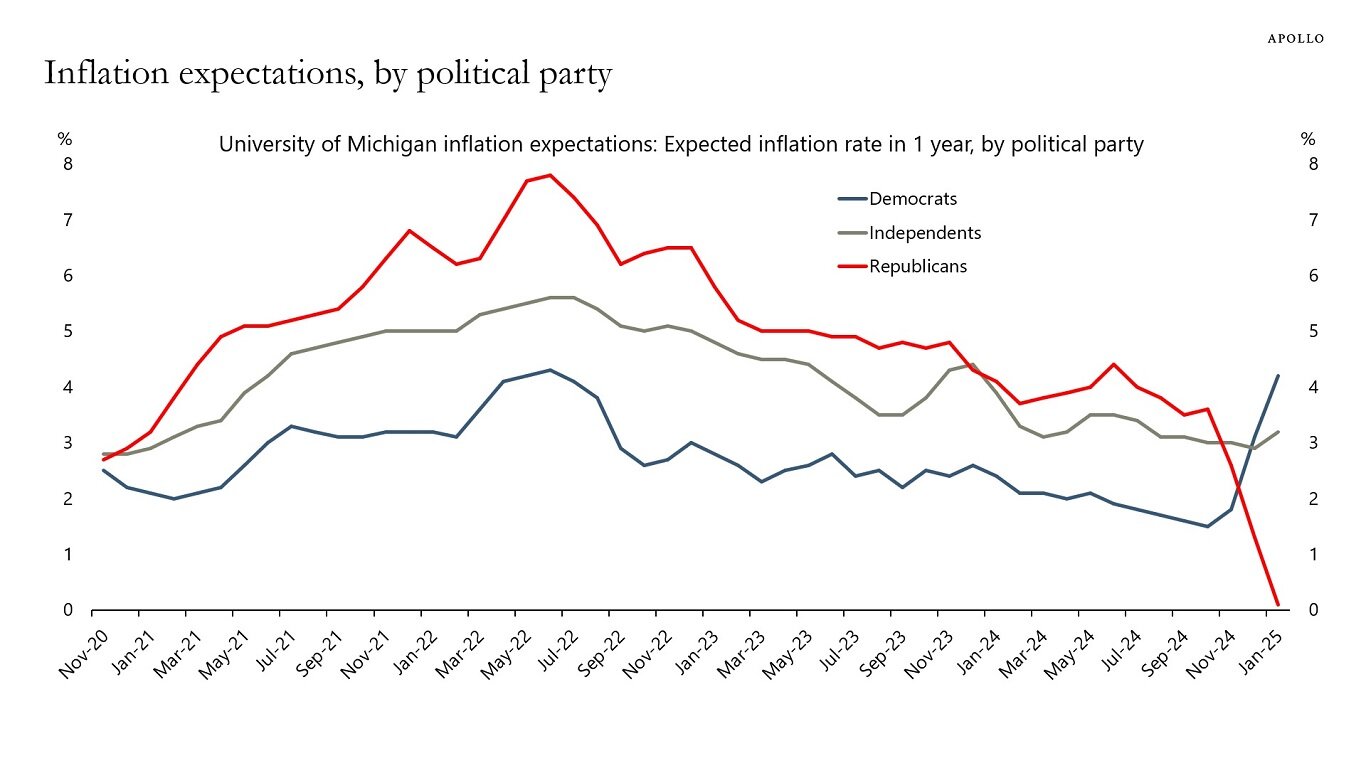

Second, recognizing our own biases is a useful trait in investing. According to the University of Michigan survey on inflation expectations, Republicans’ expectations for inflation have crashed since the election. This comes after two straight years when Republicans’ expectations for inflation were well above most official inflation metrics. Conversely, Democrats’ expectations for inflation have spiked since the election. This contrasts with the last four years when Democrats’ expectations for inflation were below most official inflation readings, with the wisest gap of expectations versus reality occurring during the summer of 2022.

Source: Apollo & Torsten Slok

We highlighted the partisan dynamics in this inflation survey as a reminder to not let politics blind us as investors, in either a bullish or bearish sense. Most experts believe that Trump is inheriting a relatively low bar when it comes to improving business-friendly economic policies. Conversely, the bar is quite high, in the opinion of the market, as to how effective his pro-growth policies might be.

It has only taken a week with President Trump back in office for us to be reminded how aggressive he is in pursuing his policy agenda. Both humans and markets alike often hate uncertainty more than bad news itself. Trump is the ultimate disruptor, and this will likely cause volatility in markets in the months and years to come.

Source: Council of Economic Advisors & Marc Andreessen

Uncertainty around Trumps policies will likely cause some uneasiness for investors at various times this year, as they are the epitome of unconventional in many ways. Having said this, many of the policies which became “normalized” over the last 15 years were moving towards an unsustainable path, most notably the trajectory of government spending.

AI capabilities are rapidly evolving and have been an increasing underpinning to the US equity markets since ChatGPT was first released in November 2022. Monday 1/27/25 seemed to be a milestone day in the evolution of AI as the Chinese startup DeepSeek launched its latest AI chatbot. The massive buzz around DeepSeek is concisely summarized by Peter H. Diamandis, MD:

Most experts do not believe DeepSeek trained their new models with the modest costs and technology which they claim. In fact, the Financial Times reports that DeepSeek likely spent over $500M on Nvidia chips, despite their low-cost claims. Regardless, even modest cost and efficiency improvements around AI are a positive development. Even Nouriel Roubini, who often finds a way to have a pessimistic viewpoint on economic issues wrote: “In my modest opinion the DeepSeek surprise / shock is – counterintuitively – over time bullish for US and global stocks as it is another positive global aggregate supply shock that increases US / global potential growth and makes exponential AI even more exponential” (source: @Nouriel).

Microsoft’s CEO Satya Nadella elaborated “Jevons paradox strikes again! As AI gets more efficient and accessible, we will see its use skyrocket, turning it into a commodity we just can’t get enough of” (source: @satyanadella).

Dan Niles, the famous hedge fund manager and founder of Niles Investment Management, shares some of his opinions on X after the DeepSeek news.

It is interesting to note that on their earnings calls on 1/29/25, Microsoft validated the narrative that their growth rate in AI spending is set to slow in the years ahead (not cutting CAPEX, but slow growth). Conversely, META said it is full speed ahead with regards to their AI CAPEX, noting that “the ability to build out this kind of infrastructure will be a major advantage” (source: @TheTranscript).

The evolution of AI is moving so rapidly even the experts seem to be having trouble keeping up. The sheer speed of progress will often leave investors with more questions than answers at times. How will the massive AI CAPEX spending ultimately be monetized (beyond the AI infrastructure companies who are the beneficiaries of the CAPEX such as NVDA, AVGO, etc.)? The estimates for increased energy sources to power the data center build outs are nothing short of staggering. But does the increased energy efficiency displayed by DeepSeek alter these estimates? What industries will most effectively use AI as a tool to increase their product offerings and their profit margins? Regardless of these questions, AI only seems to be further solidifying itself as a massive trend for the next several years. The broadening benefits of AI should be a positive development for the global economy in the decade ahead, especially given the aging demographics across the developed world.

The next few years will likely be an incredibly different market environment than the last few, and there seems to be an endless list of potential catalysts which will impact capital markets in the months ahead.

US equity markets seem to be trading in a more extreme fashion since COVID. Markets move more quickly, valuations seem to be near irrelevant over short time horizons, and speculation has become somewhat normalized across certain asset classes.

Very few investors would disagree with the claim that animal spirits are running wild at the moment, and a day of reckoning will come for some of these issues eventually. At the same time, we are in a bull market until proven otherwise and fighting the prevailing trends within markets has rarely been a profitable strategy for investors. Don Rissmiller, Chief Economist at Strategas Research Partners, recently published a report titled “The U.S. Economy Doesn’t get in big Trouble until Profits fade.” This says nothing about the direction of the next 10% move for equity markets. But it is a great reminder that bear markets and recessions occur when corporate profits are contracting, or at least flatlining. The profitability profile of corporate America is strong, despite an unsynchronized economy. Interest rate sensitive parts of the economy such as durable goods, housing, and corporate deal activity have remained depressed for the better part of the three years and could offer fresh upside catalysts.

Despite the government’s spending antics, consumer and corporate balance sheets have massively repaired themselves since 2008 and remain in solid shape today. According to JP Morgan’s Guide to the Markets, US consumers have nearly $190 Trillion of assets and $21 Trillion of liabilities. Torsten Slok of Apollo stated that the household debt to asset ratio is at a 50-year low. Slok continued to note that US nonfinancial corporate net interest payments are near record low levels.

The third year of a bull market can often be somewhat of a digestion phase for markets. At the same time, numerous sectors of the market are expected to finally experience reaccelerating earnings growth, and expectations don’t seem overly demanding outside of the US exceptionalism trade that has worked so well for the last two years.

With earnings growth on solid footing, rhetoric from policy makers, and their corresponding impact on interest rates seem to be front and center to begin this year. In this regard, it is important to note that stocks and bonds have largely become positively correlated since COVID, which is a drastic change from the prior 30+ years. Because of this, maintaining or even increasing diversification within portfolios is more important than ever. Historically, bonds are not the best asset classes when inflation levels are elevated, but they do provide ballast to portfolios for the first time in several years and could even hold their own relative to US Large Cap equities if the less optimistic forecasts from Goldman Sachs and BofA Global Research prove to be accurate in the years ahead.

We believe Uncorrelated Assets are an increasingly attractive asset class, both for diversification purposes as well as their expected return profiles. For clients with a tolerance for illiquidity, private investments should warrant serious consideration as a potential addition to portfolios.

Like many investors, we are rooting for the expected broadening of fundamentals and corresponding performance from various asset classes. Dennis DeBusschere of 22V Research recently wrote: “Historically, lower unemployment readings favor more Risk-on and Value driven internals. Combining sensitivities to unemployment and inflation, a lower unemployment rate together with stable inflation (our call) favors Energy, REITs and Financials, while Communications, Tech and Health Care underperform. Higher unemployment and inline inflation led these sector performances to reverse. Value, Deep Cyclicals and Small Caps would work relative, along with foreign markets, IF the US exceptionalism trade reverses. To be clear, we are not short the mega caps. We are just noting that the macro backdrop driving the US exceptionalism narrative (USD going straight up) is likely to be less of a tailwind as European / China growth stabilizes. Assuming our benign tariff policy outcome is correct.”

Richard Bernstein, the Chief Investment Officer at RBA Advisors, offered some interesting perspective when he mentioned that in some instances, investors have begun to view diversification as a hindrance to upside, rather than a tool to achieve financial goals.

As always, we structure portfolios to be prepared for a wide range of potential outcomes. It is cliché to say that we expect volatility in the months to come, but aside from the fall of 2023, US equity markets have been unusually calm for the last year and a half. Regardless, Warren Buffett’s steadfast optimism in regard to the long-term prospects of America serves as a great reminder regarding the mentality of a successful long-term investor, especially when short-term discomfort inevitably arises.

Sincerely,

Brian Gift, CFA

Chief Investment Officer

MBL Advisors

Bob Farrell is a legendary Merrill Lynch strategist who published his timeless list of 10 investing rules several decades ago, a version of which can be found here https://www.investopedia.com/articles/fundamental-analysis/09/market-investor-axioms.asp. It seemed some investors believed these rules were no longer as relevant as they once were when they didn’t hold true to form during the extremely abnormal bear market and subsequent recovery in 2020 and 2021. However, all of these rules seem especially pertinent today as we proceed thorough this more traditional bear market. We have written about Bob Farrell’s rules on multiple occasions in the past. But their timelessness and truth always amaze us each time we observe them.

This content was prepared by MBL Advisors and reflects the current opinion of the firm, which may change without further notice. This report is for informational purposes only and is not intended to replace the advice of a qualified professional. Nothing contained herein should be considered as investment advice or a recommendation or solicitation for the purchase or sale of any security or other investment. Opinions contained herein should not be interpreted as a forecast of future events or a guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s portfolio. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark. Commentary regarding the returns for investment indices and categories do not reflect the performance of MBL Advisors or its clients. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Investors cannot invest directly in an index.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the firm believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein. Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness, or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

This material is provided for informational purposes only. It is not an offer or solicitation to buy or sell any securities. Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. 7592033.1

Brian Gift, CFA — Chief Investment Officer — MBL Advisors

The Four Most Dangerous Words in Investing: It’s Different This Time

Equity market positioning and flows were both approaching aggressive extremes of historical ranges according to multiple gauges (sources: BofA Research Michael Hartnett; St. Louis Federal Reserve; NIAAM & Strategas Research Partners). Put/Call ratios were complacent as were put-call skews in options markets. AAII & II investor surveys remain bullish (contrarian bearish), although we are beginning to see signs of data moderating this week. In addition, there were three extremely crowded trades across capital markets before this recent correction, which could take more time to properly unwind:

When studying the history of the stock market one will quickly realize that there is rarely a “normal” environment. Rather, each market cycle has its own unique characteristics and narratives which define it and are often more obvious in hindsight. High / low inflation, high / low interest rates, geopolitics, high / low economic growth, especially accommodative / restrictive Fed policy, high / low tax regimes, large / small budget deficits, strong / weak currencies, etc. are all critical factors which influence markets over short to intermediate time frames. Regardless, of these regimes, the S&P 500 has compounded at roughly 9% +/- per year on average over the last 100 years. Sir John Templeton is famous for saying that “the four most dangerous words in investing are ‘it’s different this time.’” Nonetheless, the post-COVID environment seems unique both from an investment and economic perspective. Shutting down the economy, then dumping unfathomable amounts of fiscal and monetary stimulus into the economy and financial system, clearly produced unintended consequences, namely inflation and the “normalization” of very large debts / deficits. Unprecedented economic circumstances likely helped to accelerate some shifts in capital market dynamics over the past few years. Markets seem to move more quickly than ever as an increasing number of investors are willing to make bets with their capital for reasons other than what would be found in the Buffett / Graham investing principles playbook. The most notorious example of this is how the reddit meme stock traders began to target relatively less liquid stocks with high levels of short interest. Gabe Plotkin is one of the new owners of the Charlotte Hornets. But not long ago he ran one of the largest and most successful hedge funds on Wall Street, Melvin Capital. It is estimated that Melvin Capital lost roughly $7 Billion on their short position in GameStop stock (the Meme stock traders’ largest success). Melvin Capital was down roughly -39% in 2021 (a very good year for the stock market) and subsequently wound down its operations. This remains a truly an unfathomable event, even in hindsight. Another unique feature of the current market is how some large equity indices have become more concentrated among the heaviest weightings relative to any other point in the last 60+ years. The “Magnificent 7” stocks have effectively become their own asset class, as those 7 stocks now make up more than 30% of the S&P 500’s market capitalization and account for more than 20% of the S&P 500’s earnings. Good, bad or indifferent, these 7 stocks march to their own beat, both from a performance perspective (often uncorrelated to what the rest of the market is doing) and from a fundamental perspective (they have figured out how to grow the earnings almost regardless of the strength of the economy). Having said this, market dynamics of the “Mag 7” versus the rest of the market were becoming increasingly out of proportion at the end of the second quarter. We would even go as far to say that we were witnessing some occasional meme stock “like” behavior in some of the Mag 7 stocks, which could be observed by $2T – $3T market cap stocks moving 5% +/- in a single day, often on no real detectable news. Nvidia has been the poster child for the spectacular earnings growth driven by AI spending over the last year and a half. It has been nothing short of incredible to witness one of the largest stocks in the world grow earnings by 100%+ in a single year. At the same time, day to day market fluctuations of Nvidia’s stock have become increasingly bizarre throughout the recent months. Nvidia announced their Q1 earnings in mid May of this year, and it was a “hall of fame” earnings report, as all of their earnings announcements have been for the last five quarters . But the most amazing thing about the May earnings report was the ensuing performance of Nvidia’s stock in the weeks to come. Nvidia added over $1T in market cap during the month following this report (from mid May to mid June). For perspective, there are only six companies in the world (Mag 7 ex Tesla) who have a market cap over $1T. Notably, Berkshire Hathaway, the company that the “greatest investor of all time” has spent the last 60 years building, is not included in the list of businesses worth in excess of $1T.

The first half of 2024 was strong for global risk assets as many investors believed in the “goldilocks” narrative for the markets. US economic growth was strong, inflation continued to make progress lower, and there was an unquenchable thirst for “AI” related stocks, which seemed to go up every single day, regardless of the macro or micro news flow. The July CPI release was a day that all investors were eagerly awaiting, as it was believed that an inline / cool number would set the stage for the Fed to begin cutting rates at their September meeting. The July CPI figure was everything investors wanted and then some, but the follow-on reaction from the stock market has been anything but. Risk appetites seemed to change that day as we saw the first of many crowded trades begin to unwind. For the three weeks following, US small cap equities were the best performing asset class, and their relative outperformance was jumpstarted on the day of the CPI release, when they outperformed the NASDAQ by 5.5% on that single day. The importance of recalling this day is because it was our first glance of a crowded trade beginning to unwind. It seems that being long “high quality” in the form of secular growth stocks (i.e Mega cap tech), and short “low quality” in the form of small cap stocks was an extremely consensus trade among some institutional investors (i.e. hedge funds). This rotation continued within markets until late last week when we experienced the seemingly toxic combination of the Fed holding rates steady at their July meeting while they “wait for more data” (Wednesday), weak manufacturing data and a spike in jobless claims (Thursday), and a payroll report well below expectations on Friday. This sparked a traditional “risk off” move where all stocks and commodities (excluding gold) were sold off in equal proportions, while safe haven assets (high quality bonds) were bought heavily as interest rates plummeted. In a matter of days, narratives went from “goldilocks” to a Fed policy mistake and recession scare. Little did we know, last week was only the appetizer for what awaited global equity markets on Monday 8/5.

US equity futures traded down sharply on Sunday night as the Asian markets opened for trading on Monday 8/5. Japan was the center of attention, as their local equity markets declined by 12% – 13% that single day, due to a massive carry trade unwind. Various strategists had been noting for several weeks that short yen positioning was historically extreme, but few investors would have imagined that we would witness such a violent unraveling of this trade in a single day. Most central banks around the world began to raise interest rates in 2022 when they realized that inflation was becoming a serious issue for the global economy. However, after decades of deflation, the Bank of Japan kept their interest rates pinned around 0% in a continued effort to “reflate” their local economy. As central bank policies / interest rates began to diverge between Japan and the rest of the developed world, the Japanese Yen started to meaningfully depreciate against most other global currencies, including gold. This was the capital markets’ way of showing Japanese policy makers that there will be unintended consequences to massively suppressing interest rates. During this time, the Bank of Japan served as an endless buyer of Japanese Government bonds, in order to keep 10-year JGB yields below their stated 0.25% cap. Although the Bank of Japan was “successful” in controlling their interest rates, the consequence was that their currency was the release valve and was torched in the years to come. The Japanese Yen went from roughly 100 Yen / 1 USD in March of 2022 to around 160 Yen / 1 USD in July 2024. Large institutional investors are global players and have the sophistication to access any capital market in the world. Despite the “price of money” rapidly increasing in most currencies over the last few years, investors can still borrow Yen for close to 0%, thanks to the Bank of Japan’s extremely easy interest rate policy. Human beings always follow incentives, and thus unsurprisingly, global investors have been borrowing money from the cheapest source of capital that exists (Japan). If “free money” were not enough, investors were further rewarded by this trade when they effectively “sold” the Yen that they borrowed, and in turn bought short term government bonds in another currency. This trade was beneficial to investors in two ways. First, there was an endless supply of high-quality government bonds around the world which offered a positive “carry” relative to the investors borrowing costs. Second, most currencies have been appreciating vs. the Yen for the last few years, and this only magnified the profitability of this carry trade. However, the ultimate payoff of the Yen carry trade came to investors who bought US tech stocks (or other risk assets instead of government bonds) over the last couple of years. Shorting the Yen (on margin) to purchase US tech stocks was likely one of the greatest carry trades of all time while it lasted.

The fundamental catalyst for the unwind of this carry trade, is that the depreciation of the Japanese Yen finally reached a pain point for Japanese policy makers. Thus, the Bank of Japan began to pivot their policy stance in an effort to prioritize defending their currency. Although Japan is an export heavy economy (export economies typically like a slightly weaker currency), they import most of their energy sources (oil & natural gas) which are priced in US dollars. In other words, imports, most importantly energy sources, were becoming more expensive for the Japanese as their currency continued to depreciate. This likely became a point of legitimate pain, for Japanese citizens and businesses alike, as inflation was being imported from the rest of the world to them, serving as a tax on the economy. Over the last couple of months, the Bank of Japan has directly intervened (buying Yen: selling US dollars) in currency markets in an attempt to stop the deprecation of their currency. On numerous occasions this was only effective for a couple of days at a time, until the prevailing trend of a weaker Yen resumed. But late last week, the Bank of Japan instituted a surprise interest rate hike (just as most other central banks are beginning to cut rates) and stated that “a weak currency is a reason to tighten monetary policy.” This ignited a spark in global currency markets as the Yen began to rapidly appreciate against most other currencies. Monday August 5th was the day that the newfound Yen strength became an issue for global markets, and likely caused various investors (including Japanese citizens who were hedging against an endlessly weaker currency) to unwind a portion their carry trades consisting of short yen / long other assets (Japan stocks, US tech stocks, etc.). For highly levered players, this likely caused some forced selling / margin calls. This is likely more than many of you wanted to know about the Yen carry trade, but it sets the stage for us to attempt to think about where we go from here. As of Monday 8/5, the S&P 500 was down roughly -9% from its all-time highs from 7/16/24. Roughly 1/3 of this decline happened as US tech stocks sold off while virtually all other areas of the US equity market performed very well (but the S&P 500 is close to 50% technology related stocks now). Roughly 1/3 of this selloff occurred around the newfound growth scare / potential policy mistake by the Fed late last week. And the final 1/3 of this correction was very mechanical in nature, occurring in a single day, due to the unwinding of the Yen carry trade. Thus far, we continue to view this as a healthy and overdue correction within the context of a bull market. Corporate earnings expectations for 2024 & 2025 remain firm, and as always, will be the most important factor for equity market returns in the months and years to come.

Prior to the recent rotation out of mega cap tech names, the S&P 500 Index was more concentrated in the top 5 names than it has been at any other point in the last 60+ years. The top five names in the index (AAPL, MSFT, NVDA, GOOG & AMZN) accounted for approximately 29% of the market cap of the S&P 500. This contrasts with the top five names accounting for less than 11% of the S&P 500’s index weight at the secular lows in 1993 & 2010.

Source: @SmartReversals & Bianco Research

Excluding the last month, the historically high index concentration among the top five (29%+/-) and top ten (39% +/-) names has been an incredibly friendly dynamic to investors for the last year and half. The S&P 500 has produced very strong returns in 2023 & 2024 despite a historically low percentage of stocks achieving returns above the index returns.

Source: NDR Research & @edclissold

There have been two distinct time frames where the largest stocks have sustainably outperformed the rest of the index. These instances occurred in the late 1990’s and 2017 – 2024. As a group, the bottom 493 stocks in the S&P 500 have tended to outperform the top 7 names in the S&P 500 during other time frames over the last 50 years.

Source: NDR Research & @edclissold

A plethora of market prognosticators have mentioned how the Mag 7 stocks seem to have both offensive and defensive characteristics to them. On one hand, investors are betting that they will be some of the primary beneficiaries from the AI industrial revolution of which we are likely in the early stages. At the same time, these stocks also have fortress balance sheets (ex TSLA) and have also been the best secular growth stories in the market for ten years and running, regardless of the strength of the economy. It is difficult to debate the above facts. The biggest question investors must grapple with right now, is “how much good news” is already priced into these stocks? In mid-July, the Technology sector was trading at its highest PE ratio on record, outside of the tech bubble. These valuations will not be sustainable if profit margins begin to compress for technology stocks.

Source: Charles Schwab, @KevRGordon & Bloomberg

In their quarterly letter at the end of June, Akre Capital offered some fascinating perspective regarding part of the reason as to why it becomes difficult for the largest companies to continue to outperform indefinitely. “The S&P 500 currently boasts three companies with market capitalizations of $3 trillion or more: Apple ($3.3T), MSFT ($3.4T) and NVDA ($3.1T). The monetary value of all “final” goods and services produced by the United States – a.k.a. Gross Domestic Product or “GDP” – was $27.4 trillion in 2023. In other words, these $3 trillion+ market cap companies are currently valued at approximately 12% of GDP – each. Assume that investors in these three companies expect their market capitalizations to compound at 15% annually over the next decade. Assume US GDP growth of 3% annually over the same period. Satisfying these conditions would require the respective market capitalizations of Apple, Microsoft, and Nvidia to grow from nearly 12% of GDP today to nearly 36% of GDP by 2034. Combined, the value of these three businesses would then equate to 107% of US GDP. The sheer size of these numbers suggests to us that this outcome is unlikely. The value of any group of businesses bears some relationship to the size of the economy in which they operate. For publicly traded businesses, that relationship is called the ‘Buffett Indicator.’”

Source: Akre Capital & 22V Research

Strategas Research Partners Don Rissmiller 8/4/24 Bottom line: There’s a case the Fed should have already cut rates, but we don’t want to jump to the panic of a recession/crisis. It’s early, but the Atlanta Fed’s tracking estimate for U.S. real GDP in 3Q is running at an acceptable +2.5% q/q A.R. Productivity (which was a solid +2.3% q/q A.R. in 2Q) has been helping support growth. We believe the Fed is set to follow what other central banks are doing (eg, the Bank of England last week) and move toward a more neutral monetary policy. In anticipation, relief for interest rate sensitive sectors like housing & mfg is already starting given the rally in the bond market (the 10-year Treasury finished last week at 3.8%). Notably, U.S. pending home sales rose +4.8% m/m in July. Such rate relief & pent-up home sales should help keep the small cracks in the economy from turning into big cracks now.

Multiple “flawless” recession indicators have triggered over the past few years, including inverted yield curves, negative US Leading Economic Indicators, Manufacturing gages in negative territory, etc. These indicators caused many investors to believe the 2022 bear market was a precursor to an inevitable recession. This of course did not occur, and if / when a recession happens, it will be accompanied by its own, separate bear market. Thus, the 2022 bear market was an inflation scare, where an ensuing recession did not immediately happen. Somewhat ironically, US Real GDP has been strong, and has grown at (2%) trend growth or above for the last 6 quarters. Having said this, we are now at a point where economic growth is clearly slowing; the question is how much and how fast?

22V Research Dennis DeBusschere 8/4/24 We think the economic data will stabilize, and recession risk remains low – less low than last week, but still low. But, it won’t pay to try and monetize that view by leaning into Cyclical economic sectors and shorting Defensive and Low Vol for at least a few more weeks. In the meantime, expect a violently flat market backdrop as the sharp de-grossing/short-term oversold condition is met with continued fears of a possible recession. The Fed is going to aggressively ease and be pro-growth going forward the question is if you believe that easing will have a positive impact on economic growth longer term. We think it will. If a negative feedback loop has already started, being long Defensives makes sense. We are fading that view. Goldman Sachs 8/4/24 The chances of a U.S. recession in the next 12 months have risen from 15% to 25%, a team of Goldman economists led by Jan Hatzius said on Sunday, flagging a July employment report that looked “weak across the board.” Apollo Torsten Slok 8/4/24 There are no signs of a slowdown in restaurant bookings, TSA air travel data, tax withholdings, retail sales, hotel demand, bank lending, Broadway show attendance, and weekly box office grosses. Combined with GDP in the second quarter coming in at 2.8%, the bottom line is that the current state of the economy can be described as slowing, but still a soft landing. KKR Henry McVey 8/6/24 This ‘bump’ is not the end of the cycle, and it reminds us whey we stick to our Rolling Recovery, Rolling Recession thesis versus the traditional synchronized global recovery. From a portfolio construction perspective, we continue to remain overweight diversification, including an emphasis on non –correlated assets. Overall, though, our view is that this shock will take some time for investors to re-assume a risk on posture. Therein lies the opportunity for patient capital.

Source: Strategas Research Partners, 22V Research, Goldman Sachs, Apollo & KKR

After a couple of years of obsessing over every piece of inflation data possible, the market will no longer be as sensitive to this data (barring any large upside surprises). Economic growth is now the primary concern for market participants. The good news is that the Fed is likely to aggressively pivot and become more sensitive to their “full employment” mandate, now that their “price stability” goals have largely been accomplished. The strong labor market has been the primary reason that the US economy avoided recession over the past few years. Weekly initial jobless claims are now the single most important high frequency economic data point. Last week’s reading of 250,000 remains low by historical standards. But this data tends to trend and the 260,000 – 300,000 area will be interpreted as a warning sign for the economy.

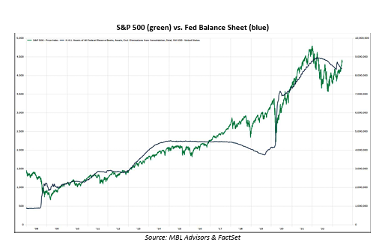

Source: MBL Advisors & FactSet

Capital Markets often have a faster and more accurate interpretation of the current investment environment than investors / strategists / economists. In this regard, the bond market is once again screaming at the Fed that they are behind the curve. This is the precise situation that occurred in the fall of 2021 when 2-year US Treasury yields started to accelerate to the upside while the Fed held rates steady at 0% and continued to conduct QE. The bond market was telling the Fed that they had a major issue with inflation, while the Fed stuck to their “transitory” thesis.

The only difference today is that yields are moving lower instead of higher, but we are back to a point where the spread between 2-year US Treasury yields, and the Fed Funds rate is historically wide.

The bond market’s message to the Fed is that they are once again behind the curve, as their policy rate is far too restrictive given the slowing growth dynamics in the economy.

Source: MBL Advisors & FactSet

The stock market’s “opinion” of the economy is certainly less optimistic than it was a couple of months ago. One of the more troubling aspects of this correction is the reality that consumer discretionary stocks are breaking down relative to the consumer staples sector, along with the broad market. This is a notable tone change relative to the last year and a half. In addition, credit spreads have begun to moderately widen, albeit from very tight levels.

Finally, most commodities outside of gold are not acting well, possibly signifying lower economic growth and inflation expectations.

These risk barometers will be important to watch in the months to come. Even in an optimistic scenario, they could be signaling that we are in more of a “late cycle” environment moving forward.

Source: MBL Advisors & FactSet

US equity markets were statistically overbought and expensive with sentiment and positioning extremely bullish before this correction started. In this regard, the recent selloff is extremely healthy thus far. Savita Subramanian noted several important statistics in her note titled “Hello Volatility” on 8/5/24.

Source: BofA Global Research & Strategas Research Partners

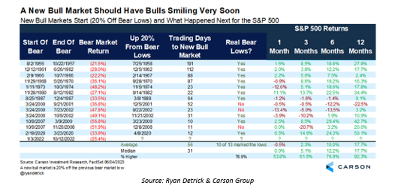

The S&P 500 remains above its upward sloping 200 day moving average, although an eventual test of this moving average will be inevitable at some point. When the S&P 500 (or any security / index) trades below its 200-day moving average, this does not necessarily mean a bear market will occur. But the bulk of the declines during major bear markets (outside of true black swan events like COVID) occur when an asset is trading below its downward sloping 200 day moving average. Fighting against prevailing trends is usually not a rewarding strategy for longer term investors.

Source: MBL Advisors & FactSet

The VIX briefly spiked to 65 on Monday morning, a level that has rarely been registered over the last 35 years. Forward Returns tend to be strong following a spike in volatility, measured by the VIX. On average, 6-month forward returns are +11.9% and are positive 81% of observations. The VIX curve is also inverted which tends to be another good contrarian buy signal. Conversely, most other oversold indicators have not yet triggered. Two opposing things are often true at the same time in this business. 6-month forward returns could be solid from these levels, despite this correction possibly needing more time to run its course, according to a plethora of other indicators. We will have more conviction that we are closer to a bottom when we begin to see a higher percentage of indicators trigger. Some of these indicators include the following:

Source: Strategas Research Partners

S&P 500 Year-over-Year earnings growth is around +11% as we approach the end of Q2 earnings season. This is clearly very respectable, and earnings growth estimates for the next several quarters remain firm. This is in stark contrast to the last year when Mag 7 companies were the only businesses who were able to grow earnings, and did so at an unbelievable clip, largely thanks to AI. A broadening out of earnings growth beyond Mega cap tech would be an extremely welcomed event for most investors. Nvidia earnings announcements have become of the most important data points for the entire market each quarter. They report Q2 earnings after the market close on 8/28.

Source: Strategas Research Partners

In summary, we are in the throes of what could be a very typical 10% – 15% correction associated with a mid-cycle slowdown. According to JP Morgan, the average peakto-trough correction since 1980 is roughly -14% (and this is skewed to the downside by some big down years such as 2008). Media outlets will explain this correction with various narratives such as a growth scare, a Fed policy mistake, the carry trade unwind, etc. All of these story lines have plenty of truth to them, but we simply believe that this market was long overdue for something more than a 4% – 5% correction, in order to flush out some of the excesses which had been building up for months. Resetting sentiment (not there yet), positioning (not there yet) and valuations (not there yet) should ultimately be healthy for extending the durability of this bull market. If we can get through this seasonally weak period for markets without too much further technical damage being done to the tape, a traditionally stronger seasonal period may await us after the election. Both in markets and in “life” more broadly, we seem to have normalized the traditionally abnormal in countless ways over the last several years. Some of the “abnormal” things which we have “normalized” include the following:

It might take a very long time for the situation in Washington D.C. to resemble normalcy. But it seems as though we are on the right path in the economy. Interest rates should settle out at more “normal” levels, which we haven’t seen since prior to 2008. Inflation will likely maintain a level in excess of the Fed’s stated 2% target, but this comes after a more than a decade of consistently undershooting that target due to deflationary pressures which persisted from the financial crisis. An economy that grows around 2% in real terms and 5% in nominal terms should be a solid environment for corporate profits. This correction could be a catalyst that returns capital markets back to a more well-balanced state of being. This would include interest rates that settle out in the 3% – 4% range, inflation in the 2% – 3% range, equity markets which produce 8% – 10% annualized returns on average, and have more broad participation beyond Mega cap tech stocks, equity market PE multiples become more palatable at something less than 20x forward earnings, winners and losers are driven by fundamentals rather than strictly if a business “has” AI or “not.” To be clear, we would not bet against the Mega Cap Tech stocks, and they consist of meaningful positions in our portfolios. Rather, we simply believe it would be emblematic of a healthy market for there to be more than one game in town. There will undoubtedly be endless surprises that come our way, as is always the case with investing. Diversification is “admitting” that we don’t “have” all the “answers” and therefore, need to be prepared for a wide range of outcomes. We look forward to discussing this with you in more detail over the days and weeks ahead.

Sincerely,

Brian Gift, CFA

Chief Investment Officer

MBL Advisors

Bob Farrell is a legendary Merrill Lynch strategist who published his timeless list of 10 investing rules several decades ago, a version of which can be found here: https://www.investopedia.com/articles/fundamental-analysis/09/market-investor-axioms.asp. We have written about Bob Farrell’s rules on multiple occasions in the past. Nonetheless, the simple brilliance of these rules always amazes us each time we observe them. They seem to be especially useful in this current environment!

This content was prepared by MBL Advisors and reflects the current opinion of the firm, which may change without further notice. This report is for informational purposes only and is not intended to replace the advice of a qualified professional. Nothing contained herein should be considered as investment advice or a recommendation or solicitation for the purchase or sale of any security or other investment. Opinions contained herein should not be interpreted as a forecast of future events or a guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s portfolio. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark. Commentary regarding the returns for investment indices and categories do not reflect the performance of MBL Advisors or its clients. Historical performance results for investment indices and/or categories generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Investors cannot invest directly in an index.

The indices referenced herein have been selected because they are well known, easily recognized by investors, and reflect those indices that the firm believes, in part based on industry practice, provide a suitable benchmark against which to evaluate the investment or broader market described herein. Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness, or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

This material is provided for informational purposes only. It is not an offer or solicitation to buy or sell any securities. Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

MBL Advisors Inc. is independently owned and operated. Investment Advisory Services are offered through MBL Wealth, LLC, a Registered Investment Advisor. Securities are offered through M Holdings Securities, Inc., a registered broker/dealer, member FINRA/SIPC. 6878005.1.

Brian Gift, CFA — Chief Investment Officer — MBL Advisors